Inside Visa’s New VAMP Ratio: How to Stay Below the Strict Thresholds

When Visa replaced its legacy dispute and fraud monitoring programs with a unified framework in April 2025, it fundamentally changed how compliance is measured and enforced across the network. The new Visa Acquirer Monitoring Program (VAMP) combines fraud and dispute activity into a single performance ratio that applies to both merchants and acquirers. That shift has already altered how risk teams, processors, and compliance managers operate.

For acquirers, the VAMP ratio creates new portfolio-level liabilities that didn’t exist under the older systems. For merchants, it introduces stricter thresholds, faster enforcement, and far less room for error. This guide outlines how the VAMP ratio works, how Visa calculates performance under the new model, and what you should do to stay compliant as thresholds tighten.

How the VAMP Ratio Works

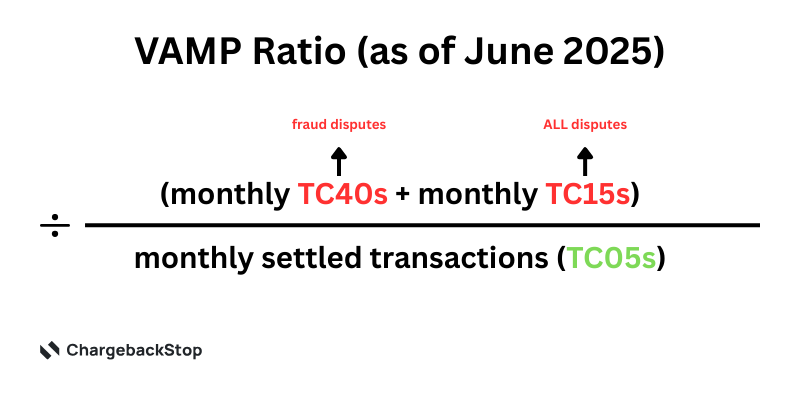

The VAMP ratio is Visa’s new standard for identifying excessive fraud and dispute activity. It replaces the separate thresholds used in the retired VDMP (Visa Dispute Monitoring Program) and VFMP (Visa Fraud Monitoring Program), consolidating them into a single formula:

Fraudulent transactions are based on TC40 data, which is issuer-reported fraud filed with Visa. Non-fraud disputes include all chargebacks except those categorised under fraud reason codes (10.xx). That’s an important distinction because under VAMP, a fraud dispute can appear twice: once as a TC40 record, once as a chargeback. The result is a higher ratio than merchants may be used to under the older programs.

Visa excludes a small set of dispute types from this calculation. RDR-resolved disputes, for example, do not count. Neither do disputes that are successfully overturned using Compelling Evidence 3.0. If a fraud claim is proven false, the related TC40 record may also be suppressed, though this depends on issuer acceptance.

For merchants used to monitoring chargeback rate alone, the jump to VAMP can feel abrupt. A business that previously sat just below the 0.9% VDMP limit could now exceed 1.2% or more under VAMP, without any increase in actual disputes. That discrepancy is the byproduct of merging two metrics into one. And it’s why so many merchants found themselves receiving advisory notices after the April 2025 rollout.

Thresholds, Timelines, and Fines

Visa began enforcement of the VAMP ratio in stages. The official launch date was April 1, 2025, when the VDMP and VFMP programs were retired. For the first six months, Visa operated in advisory mode, whereby merchants and acquirers exceeding the new thresholds received warnings but were not fined. That grace period ended on September 30. From October 1, fines are active.

For the remainder of 2025, the merchant threshold for VAMP is 1.5% (provided the merchant also receives at least 1,000 combined fraud and dispute cases in a month). For acquirers, the threshold is 0.5%, calculated at the portfolio level.

On January 1, 2026, thresholds tighten further:

- The merchant threshold drops to 0.9%.

- Acquirers will be held to two levels: portfolios above 0.3% are considered "Above Standard," while anything above 0.5% is flagged as "Excessive."

Fines apply once an entity is officially enrolled in the VAMP program. Acquirers are billed $10 per fraud or dispute event falling in the “above threshold” category and may pass those fines to their merchants. Merchants exceeding the ratio are expected to submit a remediation plan, and if their ratio does not fall within 90 days, fines begin to apply at the same rate: $10 per excessive event.

Why Merchants Are More Exposed

VAMP may be positioned as an acquirer monitoring program, but the merchant bears the operational burden. Acquirers are now directly liable for dispute and fraud activity across their portfolios, and that liability flows downstream. We’re already seeing acquirers impose merchant-level limits below Visa’s thresholds to buffer their portfolio average.

That means a merchant at 1.2% today may be dropped by their acquirer, even though Visa won’t enforce fines until they hit 0.9%. In other words, you don’t need to break Visa’s rules to lose processing access. You just need to jeopardize your acquirer’s ratio.

Visa’s removal of Early Warning tiers also shortens the timeline. Merchants no longer receive an alert at 0.65% or 0.85%. Unless your acquirer provides its own advance notice, your first official signal could be a program enrollment letter.

How to Stay Below the Line

Reducing chargebacks alone won’t keep you compliant under VAMP. You need to reduce fraud claims, prevent disputes from reaching the network, and make sure your operational and billing practices don’t drive repeat complaints. That starts with four core areas:

1. Prevent Fraud Before It Happens

Any transaction flagged as fraudulent by an issuer and reported to Visa contributes to your VAMP ratio, whether or not a chargeback follows. That makes fraud prevention a primary compliance function. Start by strengthening front-end controls by deploying 3-D Secure on risky transactions, setting up velocity limits, and implementing device fingerprinting.

Keep in mind that not all fraud is technical. A surprising amount of “unauthorized” fraud stems from operational gaps like delayed fulfillment, confusing descriptors, or a lack of post-purchase communication. Make sure customers recognize your billing label, get notified when their order ships, and can easily track their delivery status. The more uncertainty in your transaction flow, the more likely a legitimate customer flags it as fraud.

2. Resolve Disputes Before They Count

Disputes that reach the chargeback stage impact your VAMP ratio, but not every customer complaint has to escalate that far. Visa’s Rapid Dispute Resolution (RDR) allows merchants to proactively refund specific types of disputes before they become chargebacks.

You can set up rules to auto-refund disputes under a certain dollar amount, for select reason codes, or within a defined time window post-transaction. These refunded transactions never hit your chargeback count and never show up in your VAMP math.

3. Use Compelling Evidence 3.0

CE 3.0 is a key weapon against friendly fraud, allowing merchants to overturn fraud claims by demonstrating that the customer previously made legitimate, undisputed purchases under the same account credentials. To qualify, you typically need to show at least two historical transactions that match key data points: customer email, device ID, IP address, or login pattern.

When a CE 3.0 submission is accepted, not only is the chargeback reversed, but the associated TC40 fraud report may be suppressed as well. That’s a double win for your VAMP ratio.

4. Monitor Your Ratio

You can’t fix what you can’t measure. The VAMP ratio includes both chargebacks and issuer-reported fraud, so relying on traditional chargeback alerts alone will leave blind spots. Merchants need a combined view of chargebacks and TC40 activity, updated frequently and tracked against Visa’s thresholds, ideally with alerts when monthly velocity exceeds safe levels.

This is especially critical for acquirer relationships. Your processor is watching your performance as closely as Visa is, and if you start trending above 0.7%, expect increased scrutiny. Build your own internal monitoring into weekly workflows. Flag shifts in reason codes, identify repeat offenders, and correlate fraud reports with specific products or campaigns.

Keep Your VAMP Ratio in Check with ChargebackStop

ChargebackStop helps merchants and acquirers stay compliant with VAMP by integrating fraud intelligence, chargeback alerts, and pre-dispute resolution tools into one platform. We provide:

- Real-time VAMP ratio tracking (including TC40 ingestion)

- RDR setup and automated dispute filtering

- CE 3.0 evidence management

- Custom alert thresholds and acquirer reporting tools

Whether you’re a merchant trying to avoid fines or an acquirer managing portfolio risk, ChargebackStop gives you the data and automation needed to stay below Visa’s limits without guesswork.

Book a demo to see how we help you prevent chargebacks before they happen, and protect your access to Visa processing under the new rules.