Chargeback Prevention

Your Guide to Stopping Chargebacks Before They Happen

The complete, go-to guide for everything that merchants need to know about

disputes and chargeback prevention in 2026.

Chargeback Prevention in 30 Seconds

Chargeback prevention is the work done to stop disputes from becoming chargebacks. That includes reducing the reasons customers go to their bank in the first place, and intercepting disputes early when issuers give merchants the chance to resolve them before fees, ratios, and monitoring programmes are triggered. It sits upstream of representment and focuses on volume, not win rates.

This page breaks down how chargeback prevention works, where merchants lose control, and what tactics consistently reduce dispute volume. It covers the most common chargeback drivers, prevention methods, and how network tools like alerts fit into a wider prevention strategy.

If you’re trying to lower ratios, avoid monitoring programmes, or spend less time reacting to disputes, this page is your starting point!

Top Resourcesin Chargeback Prevention

When Refunds Fail: Transaction Lifecycle Errors That Escalate Into Chargebacks

Verifi RDR, CDRN, and Ethoca Alerts: Choosing The Right Tool for Each Dispute Type

8 Reasons Card Holders Say They Don’t Recognize a Transaction

The Excessive Chargeback Merchant (ECM) Program: What Merchants Need to Know

What is Chargeback Prevention?

Chargeback prevention is a catch-all term for everything a merchant does to stop disputes from turning into chargebacks in the first place. That includes how you market and sell, how you authenticate customers, how clearly you bill them, how fast you ship, how you handle complaints, and how you respond when a bank signals that a customer is unhappy.

What it isn't, as many believe, is a single tool or program. Rather, it’s the set of processes, data, and decisions that sit between “customer has a problem” and “issuer files a chargeback.”

For most merchants, prevention work shows up in three places:

- Upstream, where you decide which orders to accept and how you set expectations.

- In the middle, where customer service either resolves issues or lets them fester.

- Downstream, where pre-dispute alerts and network tools give you a short window to fix things before they hit you hardest.

The ultimate, gold-standard goal with chargeback prevention is fewer disputes escalated to the networks, which translates to lower chargeback ratios and less time spent firefighting. To get there, you need a clean understanding of what a “dispute” is in card-network terms, and where prevention actually sits relative to representment.

What's the Difference Between Disputes vs Chargebacks?

“Chargeback” and “dispute” are often used interchangeably, but they describe different points in the process.

A dispute starts when a cardholder questions a transaction with their bank. That can happen in-app, online, or via a call centre, and the issuer reviews the claim against its rules and the network’s framework. At this point, the original transaction is still intact on the merchant side because the bank hasn’t reversed anything yet.

A chargeback is the formal reversal of funds after the issuer decides to push the claim through the network. The transaction amount is debited from the acquirer and, in turn, from the merchant. A chargeback comes with a fee, counts against your ratio, and opens the door to monitoring programs and potential fines.

Chargeback prevention focuses on the gap between the first dispute and the chargeback being filed.

- Before the dispute: Can you stop the issue arising at all through better fraud controls, clearer expectations, or cleaner ops?

- After the dispute but before the chargeback: If the issuer participates in alerts or automated programs, can you resolve the case (refund, clarify, cancel) so it never becomes a chargeback?

Once a dispute becomes a chargeback, you’re no longer preventing but recovering. At that point, the question shifts from “How do we stop this from hitting us?” to “How do we deal with the loss that’s just landed?” — and that’s where recovery and representment will usually come apart.

What’s the Difference Between Recovery vs Representment?

From the moment a chargeback is raised, you only have two broad ways to respond:

- accept the loss and write it off (and absorb the hit to your ratios); or

- try to claw the money back.

Everything you do in that phase sits under chargeback recovery. That includes issuing a refund before a second cycle, negotiating with a customer, or using network tools and your acquirer to resolve cases. It is the umbrella term for any action you take to reduce the financial impact once the chargeback exists.

Chargeback representment is one specific recovery tactic that falls under the umbrella. It’s the formal process of contesting a chargeback with evidence. You assemble an argument that the transaction was valid and send it back through the acquirer to the issuer. If the issuer accepts your case, the funds are reinstated. If they don’t, the dispute can move into further cycles and, eventually, arbitration.

There are a few practical differences between the two:

- Scope: Recovery can mean issuing a refund at the alert stage, offering a partial credit to close a complaint, or accepting some disputes as cheaper to lose. Representment only applies once a chargeback has been filed with the scheme.

- Effort vs impact: A refund or write-off is usually quick but locks in the loss. Representment is slower and evidence-heavy, but it’s the only way to reverse a chargeback that’s already on your MID.

- Use case: Recovery decisions are portfolio-level questions: which disputes do we absorb, which do we auto-refund, which do we fight? Representment is the case-by-case execution of the “fight” bucket.

In short, prevention is about shrinking the number of disputes that ever reach this point, whereas recovery is about what you do when they do. Representment is the sharpest tool in that recovery kit, and because it’s expensive in time and attention, you only reach for it when the evidence and costs justify it.

Why Does Chargeback Prevention Matter for Merchants?

Chargebacks aren’t just a line item on your balance sheet. They shape margins, dictate how much work your team has to do, and, if worst comes to worst, ultimately decide how long you get to keep your merchant accounts.

Chargeback prevention matters because it changes all three:

- It cuts the true cost per dispute, not just the face value of the transaction.

- It stops chargebacks from soaking up time and attention across support, finance, risk, and ops.

- It keeps your chargeback ratios low enough that acquirers and schemes stay comfortable instead of reacting with monitoring and fines.

When you look at chargebacks this way, prevention becomes a core part of how you protect revenue and account health.

What is a Chargeback Ratio?

Card networks and acquirers don’t just care how many chargebacks you have. They care about how many you have relative to your successful transactions. That percentage is your chargeback ratio, and it carries more weight in their decision-making than any individual dispute.

The True Cost of Chargebacks for Merchants

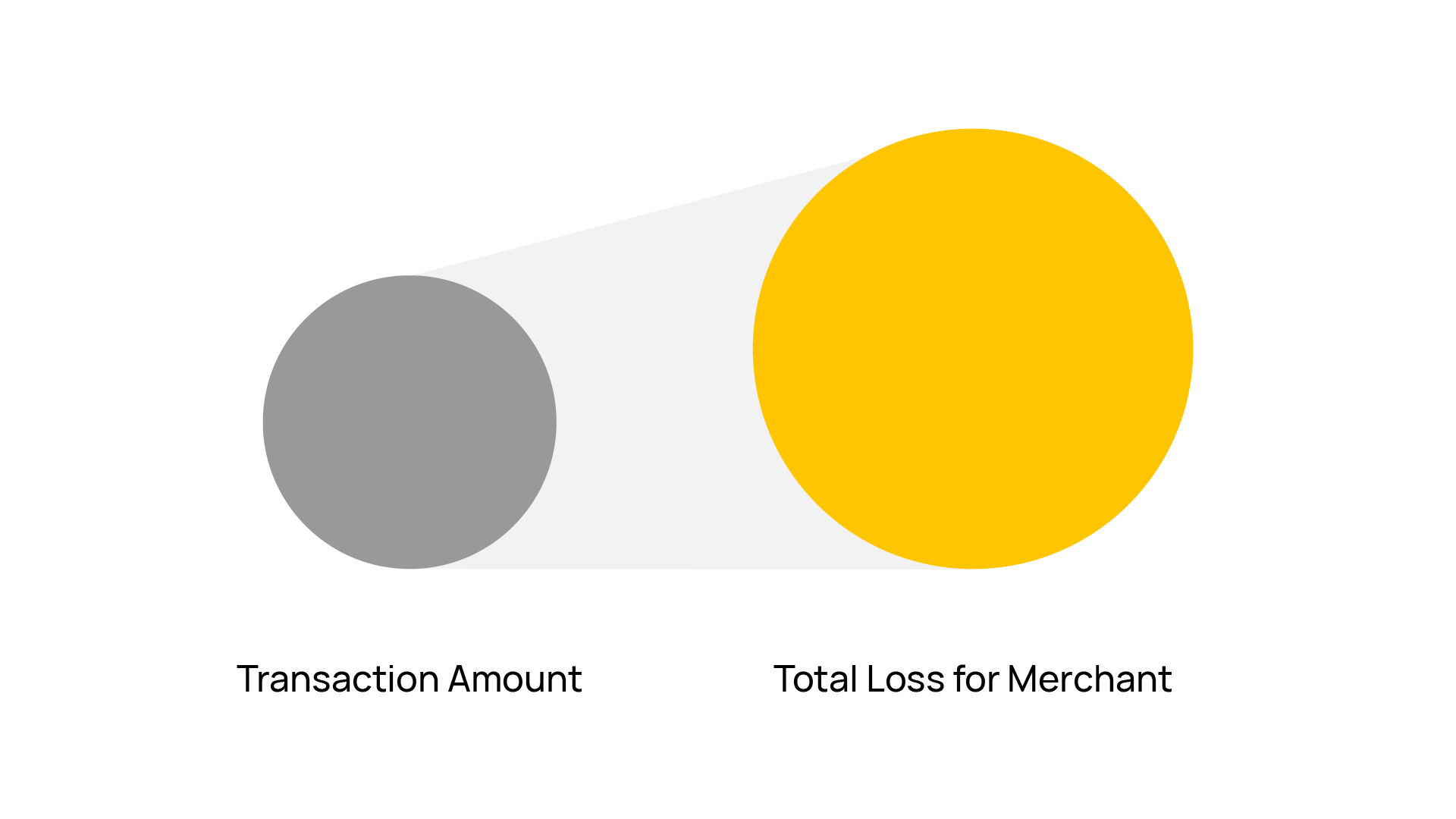

Chargebacks might sound pretty simple on the face of it. What's complicated about the customer getting their money back? Sure, it comes with a fee for you, but that's the end of it, right? Well, not exactly. The reality is much messier because every chargeback typically rolls up several layers of loss:

- The transaction amount: the sale is gone.

- The product or service: you don’t always get it back, especially digital goods.

- The chargeback fee: enough to wipe out the margin on the order.

- Internal handling time: someone in your team still has to read the notification, pull data, log the loss, and decide what to do next.

On top of that, there’s the impact you don’t see. You’ve spent money to acquire that customer. If their first instinct is to go to the bank rather than to you, you’ve probably lost their future revenue as well. If the root cause was something avoidable such as late delivery or a clumsy refund experience, the business is paying twice: once in dispute costs, once in churn.

Prevention tackles the problem at the point where it is still cheap. Stopping a bad order at checkout, resolving a complaint before the customer calls their bank, or auto-refunding a dispute in the pre-chargeback window costs a fraction of what it takes to fight or absorb a fully-formed chargeback.

How Chargebacks Impact Revenue, Ops, and Risk

Once chargebacks reach a certain volume, they begin taking a serious toll on how the business operates. On revenue, recurring chargebacks act like a tax:

- Fees and write-offs eat into margins.

- Processors respond with higher pricing or rolling reserves.

- Teams become wary of otherwise attractive customer segments because they “always dispute”, which nudges product decisions in the wrong direction.

They’re also a massive drag operationally. Support teams juggle customers threatening to go to their bank, finance spends hours reconciling debits, credits, and fees that shouldn’t have existed, and risk teams live in triage mode instead of fixing root causes.

Then there’s the risk view. Issuers and acquirers look at dispute performance as a core signal. As your chargebacks climb, you stop looking like a standard merchant and start looking like a potential liability. That can mean closer monitoring and far less patience if something else goes wrong.

Chargeback prevention cuts across all three areas at once. Fewer chargebacks means healthier margins, lighter workloads, and a risk profile your banking partners are comfortable supporting.

5 Chargeback Prevention Challenges in 2026

Most merchants aren’t dealing with one type of chargeback. Disputes tend to cluster in a few predictable places, such as how customers behave and where your own processes crack under pressure. Right now, most portfolios see the bulk of their chargebacks coming from five areas.

1. Friendly Fraud and First-Party Misuse

Friendly fraud is the uncomfortable middle ground where the payment is legitimate, but the dispute isn’t. You see it when cardholders:

- Claim that a genuine purchase was unauthorised.

- Say something never arrived despite delivery and usage records.

Sometimes it’s deliberate abuse, sometimes it’s confusion or buyer’s remorse. Either way, the issuer is pulled in before you are, and the dispute arrives looking “clean” from the bank’s point of view. Prevention here depends on things like recognisable descriptors, clear policies, easy ways to contact you, and a way to intercept disputes early rather than chasing them after the fact.

2. Fraud-Driven Chargebacks

Fraud-driven chargebacks are the result of transactions that should never have been approved. Stolen credentials, account takeover, synthetic identities, aggressive testing on your checkout — it all turns into unauthorised-use disputes a few days or weeks later. You’ll see patterns around specific BINs, regions, devices, or traffic sources.

This is where front-end controls do the heavy lifting: layered fraud screening, step-up authentication where it makes sense, and rules that let you tighten the net on risky traffic while keeping good customers flowing. Prevention here comes down to whether your fraud controls are doing enough work before the payment is captured:

- Are you applying stronger checks where the risk is clearly higher?

- Is authentication being triggered intelligently, rather than bluntly across all traffic?

- Are rules and thresholds being reviewed as fraud patterns change, or left untouched for months at a time?

The goal isn’t to completely eliminate fraud; that’s impossible. It’s to make sure that obvious fraud doesn’t make it through unchecked and turn into chargebacks.

3. Fulfilment and Refund Failures

A significant share of chargebacks still comes from issues that were completely under the merchant’s control, such as late shipments, missing items, damaged goods, refunds promised but not processed, or simple billing errors. These disputes tend to show up as:

- “Goods/services not received.”

- “Goods/services not as described.”

- “Credit not processed.”

In most of these cases, the cardholder could have been kept away from their bank if communication, fulfilment, or refunds had been handled differently. The prevention work here sits in improving how orders are fulfilled, how exceptions are communicated, and how quickly refunds are pushed through once agreed.

4. Subscriptions and Recurring Billing Risks

Subscription and recurring businesses have a different headache in the form of disputes over things like renewals, trials that rolled into paid plans, and long-forgotten services that show up on a statement months later. Typical triggers include:

- Trials that convert into paid subscriptions with no renewal reminder.

- Cancellation flows that are hard to find or slow to action.

- Several transactions disputed all at once when a customer finally notices.

You don’t fix this with fraud tools but with honest sign-up flows, clear billing schedules, proactive reminders, and cancellations that work on the first attempt. We unpack that in more depth in our dedicated guides for SaaS and subscription merchants.

5. Digital Goods Disputes

For digital goods, the dispute pattern shifts again. Delivery is instant and intangible, which makes “I never received it” or “someone else must have used my card” harder to prove wrong. Digital merchants are often hit by:

- Chargebacks on content that has clearly been accessed or consumed.

- In-app and in-game purchases that are disputed after use.

- Access issues where the customer never figured out how to log in or download, and went straight to their bank.

Prevention here relies on stronger upfront consent, clearer messaging around billing, solid telemetry (access logs, downloads, IP/device data), and a playbook for resolving access problems quickly through support.

Getting a Grip on Digital Goods Disputes

Digital products don’t ship, can’t be returned, and often get consumed instantly. That makes disputes harder to prevent and even harder to unwind once a customer goes to their bank. From “item not received” claims to post-use disputes, digital merchants face a very different chargeback profile to physical goods sellers.

Preventing Chargebacks Doesn’t Need to be Complicated

Most chageback prevention efforts fail because they try to do everything at once. The merchants that actually bring their numbers down tend to focus on a small set of simple controls and get those working properly before layering on anything else.

The four methods below cover the bulk of preventable disputes across most merchant models. These are the controls that consistently reduce chargeback volumes when they’re implemented with intent and taken seriously.

Intercept Disputes Before They Escalate

The one thing you want to avoid at all costs is a chargeback being filed into card network schemes, because once they’re there, the damage is already done. Fees apply immediately, and your ratios take a hit. Even if you succeed in representment, it still counts as a chargeback event.

The earliest practical intervention point is after a cardholder contacts their bank but before the dispute converts into a chargeback. For participating issuers, alerts and automated network programmes notify merchants of that moment, and, when used properly, they let you resolve the issue before it ever hits your account. We’ll explore these pre-dispute alerts in more detail later.

Reduce Fraud at Checkout

Fraud-related chargebacks are the result of approvals that shouldn’t have happened. When unauthorized transactions get through, they almost always return as disputes later. The delay hides the cause, but the link is usually obvious in hindsight, with familiar patterns across devices, regions, payment details, or traffic sources.

Prevention here sits at the point of approval. That means reviewing how fraud checks are applied, how often rules are revisited, and whether higher-risk traffic is actually being treated differently. Static controls tend to decay quietly, because everything looks fine until the chargebacks arrive.

Improve Billing Transparency

Many chargebacks begin with a customer not recognizing your charge. That might be because the descriptor is unclear, the billing name doesn’t match the brand the customer remembers, or the timing of the charge wasn’t obvious at checkout. From the cardholder’s point of view, disputing the transaction feels safer than guessing. It’s also faster.

Clear billing doesn’t stop every dispute, but it removes a large and avoidable trigger. When customers can immediately identify a charge and know how to contact you, far fewer of them default to their bank. This is one of the least technical prevention fixes, and one of the most consistently effective.

Strengthen Customer Support

When customers can’t get answers from you, they look for them elsewhere. Unfortunately, banks are always available.

Support plays a direct role in chargeback prevention because it determines whether frustration is resolved or escalated. Slow responses, vague replies, or unresolved tickets push customers toward disputes even when the underlying issue probably isn’t worth a dispute.

Effective prevention here doesn’t require perfect support coverage, but you do need to ensure you’re offering clear support paths with reasonable timelines for resolution. Customers are far more likely to wait when they understand what’s happening and believe someone is dealing with it.

Pre-Chargeback Alerts and Network Prevention Tools

Most merchants won’t know about a problem until it has already become a chargeback, and by that point, the scenes are involved. Pre-chargeback tools to shift that moment of realization to earlier along in the process by giving you visibility into disputes while they’re still forming, when the cheapest and cleanest outcome is often to resolve the issue and move on.

What Are Pre-Chargeback Alerts?

Pre-chargeback alerts are notifications triggered when a cardholder contacts their bank to question a transaction, before the issuer files a chargeback through the network.

From a merchant perspective, this is the most valuable window in the entire dispute lifecycle. The transaction hasn’t been reversed yet, no chargeback fee has been applied, and nothing has hit your ratios. You still have scope to decide how to handle the case.

Alerts simply give you a heads up that a customer is unhappy enough to involve their bank. What they don’t tell you is whether the dispute is valid or winnable. In most cases, however, simply knowing a dispute is coming is enough because a fast refund or clarification at this stage can prevent the dispute from ever turning into a chargeback.

Not all issuers participate, and alerts don’t cover every scenario. But where they are available, they consistently reduce volume by removing low-value, low-context disputes from the system before they escalate.

Verifi Rapid Dispute Resolution

Verifi Rapid Dispute Resolution (RDR) is Visa’s automated pre-chargeback resolution programme.

RDR works by applying merchant-defined rules to incoming disputes. When a cardholder raises an issue with a participating issuer, Visa checks those rules and decides whether the dispute should be resolved automatically. In practice, that usually means issuing a refund before a chargeback is created.

The key point with RDR is that you are not reacting case by case. You decide in advance which types of disputes you’re willing to resolve automatically and on what terms. That might include low-value transactions, specific reason codes, or disputes that fall within a certain time window.

Used intelligently, RDR takes predictable, low-signal disputes out of your workflow entirely. Instead of reviewing them, representing them, or arguing with issuers, they’re closed quietly before they affect your account. Used badly, however, and it can turn into an indiscriminate refund engine; the difference comes down to how deliberately the rules are set and reviewed.

Ethoca Alerts

Ethoca by Mastercard operates on a similar principle but with a different delivery model.

When a participating issuer receives a dispute, Ethoca sends an alert directly to the merchant or their service provider. You then have a short window to act before the chargeback is filed. That action is usually a refund, but in some cases it may involve contacting the customer or correcting an obvious error.

Unlike RDR, Ethoca Alerts are not fully automated by default. They require a decision for each alert, which makes them better suited to dispute scenarios where you want tighter control over which disputes are resolved early.

For many merchants, Ethoca handles the long tail of disputes that don’t fit neatly into automated rules. Combined with network programmes like RDR, it allows you to split pre-chargeback handling into two streams: disputes that should always be resolved early, and disputes that deserve a closer look.

Keep in mind that while powerful, these tools don’t eliminate chargebacks entirely. What they do — and do very well — is change the shape of your dispute volume, removing the noisiest, least valuable cases before they reach the schemes and leaving you with a smaller, more intentional set of disputes to deal with downstream.

Chargeback Monitoring Programs

Chargeback monitoring programs are the reason why prevention isn’t optional. These are the mechanisms that card networks use to flag merchants whose dispute levels suggest a systemic problem. Once you’re enrolled, chargebacks begin to drive serious financial and operational consequences.

The requirements, thresholds, and consequences vary by network, but they all have the same underlying goal to identify merchants with high chargeback volumes and levy penalties against them. The two main ones are Visa’s VAMP and Mastercard’s ECM/HECM programs.

The Visa Acquirer Monitoring Program

Visa’s monitoring framework is built around the Visa Acquirer Monitoring Program, usually shortened to VAMP, which came into force in 2025 when it replaced VDMP and VFMP.

VAMP looks at your chargeback ratio and absolute dispute counts over defined periods, and if your numbers cross Visa’s thresholds, your acquirer is required to step in. That can mean increased reporting, formal remediation plans, and, if the situation persists, financial assessments layered on top of your existing fees.

The important thing for merchants to understand is that VAMP is not triggered by a single bad month, but by consistent patterns. A slow leak of preventable disputes can push a business into monitoring just as effectively as a sudden spike in fraud.

Once you’re enrolled in VAMP, the clock starts ticking, and Visa expects to see improvements quickly. If ratios stay elevated, the more expensive and restrictive things become. Prevention is what keeps you out in the first place, but when you’re in, early intervention is what gets you back out.

What is Visa VAMP?

Visa’s Acquirer Monitoring Program is a new framework for monitoring fraud and chargebacks across the payment ecosystem. Effective April 1, 2025, and enforced from October 1, 2025, it replaces VDMP and VFMP, unifying how acquirers and merchants are managed when dispute and fraud levels are too high.

Mastercard ECM and HECM

Mastercard operates a similar system through its Excessive Chargeback Program, split into two tiers: Excessive Chargeback Merchant (ECM) and High Excessive Chargeback Merchant (HECM).

ECM is the entry point for merchants whose chargeback levels have exceeded Mastercard’s acceptable range, and for whom corrective action is required. HECM is the escalation tier, reserved for merchants whose ratios remain high or continue to worsen.

The shift from ECM to HECM is extremely punitive: reporting requirements increase, assessments grow, and acquirers become far less tolerant of slow progress. Merchants want to avoid HECM at all costs because once you get to that stage, Mastercard has real and serious doubts about whether the merchant can realistically bring disputes under control.

As with VAMP, the path into these programmes is often paved with small, repeated failures rather than a single catastrophic event. That’s why prevention work focused on volume — not just win rates — matters so much in the Mastercard ecosystem.

What Happens When Ratios Get Too High?

When chargeback ratios rise past network thresholds, merchants typically face some combination of:

- Mandatory monitoring and remediation plans overseen by their acquirer.

- Additional per-chargeback assessments on top of existing fees.

- Increased reserves or delayed settlements.

- Restrictions on processing volume or business models.

- In severe cases, termination of the merchant account and placement on industry watchlists.

At that point, even “winning” disputes through representment doesn’t undo the damage, and that's why chargeback prevention has truly earned its keep. By reducing the number of disputes that ever convert into chargebacks, you lower the metric that the networks actually care about. That keeps monitoring programmes from being triggered in the first place, and, if you’re already enrolled, gives you the fastest route back to stable ground.

Tools and Approaches to Chargeback Prevention

There’s no shortage of ways to “do” chargeback prevention. The difference is whether those approaches actually reduce volume or just rearrange the work. Most merchants end up combining tools, processes, and people into a process that works for them.

Chargeback Prevention Software

Chargeback prevention software exists to deal with the parts of the process that don’t benefit from human judgment. At its best, software handles things like:

- Receiving dispute and alert data directly from the networks

- Matching alerts to transactions without manual reconciliation

- Applying consistent rules to predictable cases

- Tracking ratios and trends before they become a problem

As we’ve discussed, prevention is time-sensitive, and pre-chargeback alerts have a short window, so the more streamlined you can make your ops with the right software, the better. If teams are relying on inboxes, spreadsheets, or processor portals, things can easily get missed.

Manual Processes vs Automation

Manual prevention tends to grow organically: Someone watches reports, someone else checks alerts when they remember, and refunds get issued after a few internal messages. This works just fine at low volume, until it doesn’t.

The problem isn’t that manual processes are wrong, but they just don’t scale well. As your dispute volumes grow over time, delays creep in, decisions become inconsistent, and the same type of dispute gets handled three different ways depending on who sees it first.

Introducing automation makes it easier for you to handle growing volumes where outcomes are already known. If you’ve learned that certain disputes are never worth fighting, or that some refund scenarios almost always escalate if left alone, there’s little value in re-deciding that every time.

A practical split usually looks like this:

- Automated handling for low-value, repeatable, low-context disputes

- Manual review for edge cases where evidence or customer history matters

The goal isn’t to remove humans from the loop, but to stop wasting them on work that doesn’t need judgment.

In-House Teams vs Outsourced Prevention

Many merchants start by keeping everything in-house. We get it, it feels safer, and it keeps knowledge close to the business. Over time, however, there are trade-offs because running prevention internally means:

- Hiring or training people who understand network rules

- Keeping up with programme changes and deadlines

- Absorbing the operational cost even when volumes spike

For some teams, that makes sense. For others, prevention becomes a background task that competes with fraud, support, finance, and compliance.

Outsourced prevention shifts that burden. Instead of building and maintaining specialist expertise, merchants lean on a provider whose entire job is to keep disputes from escalating and ratios from drifting. Merchants that outsource prevention usually do it because chargebacks aren’t their core business, but the consequences still land on them when things go wrong.

In practice, the most effective setups mix approaches, with internal ownership of policy and thresholds, supported by software and external expertise that handle execution at scale.

How ChargebackStop Supports Chargeback Prevention

ChargebackStop is built around the idea that prevention should happen as early as possible, with as little manual effort as possible. Our platform focuses on catching disputes before they become chargebacks, reducing avoidable volume, and giving teams clear visibility into what’s actually driving their numbers.

Real-Time Pre-Dispute Alerts

ChargebackStop provides direct access to network alerts from Ethoca and Verifi, so disputes surface while they are still in the pre-chargeback stage. Alerts are automatically matched to transactions, giving teams immediate context and the ability to resolve issues before fees apply or ratios are affected.

Automated Resolution Rules

ChargebackStop allows merchants to define resolution rules for predictable disputes. The platform automatically detects duplicates or invalid alerts, credits them, and applies configured actions such as refunds or cancellations. This removes low-value, repeat disputes from the workflow without requiring manual review.

Fraud and Dispute Visibility

ChargebackStop centralises pre-dispute alerts, chargebacks, and network fraud notifications in a single dashboard. This gives teams real-time visibility into dispute and fraud patterns across products, payment methods, and regions, helping issues surface early rather than after ratios have already moved.

Managed Support When Prevention Fails

When disputes do convert into chargebacks, ChargebackStop offers a managed recovery service that handles evidence collection, pack building, submission, and tracking. This keeps your internal teams focused on prevention, while recovery is handled consistently and in line with network requirements.

Getting Started with Chargeback Prevention

Chargeback prevention gets overwhelming when teams try to fix everything at once. The fastest progress usually comes from tightening a few obvious gaps, then deciding where it makes sense to systemise the work.

What to Fix First

Start with the things that generate disputes quickly and repeatedly.

If you look at your recent chargebacks, you’ll probably notice some patterns. Maybe some of your refunds took too long, or some of your customers had renewals they didn’t expect. Perhaps some of your customers aren’t recognizing your billing descriptor or receiving replies from customer support. These are very easy fixes that lead to instant wins:

- Clean up billing descriptors so customers recognise charges.

- Make refund policies easy to find and refund timelines predictable.

- Checking whether disputes are arriving that could have been intercepted with alerts

Getting these things right reduces dispute noise and buys you space to work on a more solid, structural prevention strategy.

When to Add Automation or Outsourcing

Automation and outsourcing make sense once prevention work starts competing with everything else your team is responsible for.

If alerts are being missed, refunds are being issued inconsistently, or chargebacks are only reviewed once ratios have already moved, manual processes are probably stretched too thin. That’s usually the point where automation starts preventing avoidable damage.

Many merchants choose to keep policy and decision-making in-house, while handing execution to systems or specialists who deal with disputes all day, every day, and that’s exactly what you can do with ChargebackStop.

Put chargeback prevention on autopilot

See how early alerts, automation, and managed recovery fit into your existing payments setup, and what it would take to reduce disputes without adding operational overhead.

Chargeback Prevention FAQs

Straight answers to the questions merchants actually ask about chargeback prevention.

No. Pre-chargeback alerts surface disputes before a chargeback is filed with the schemes. If you resolve the issue at that stage, usually by refunding, no chargeback is created, and nothing is added to your ratio. That’s the main reason alerts are so valuable: they let you reduce volume without taking a ratio hit.

No, and anyone claiming otherwise is selling something!

Some chargebacks are the result of genuine fraud, issuer decisions, or edge cases you can’t control. Prevention is about reducing the avoidable portion that stems from confusion, timing issues, low-value friendly fraud, and operational failures. That’s where most merchants see meaningful gains.

There isn’t a single tactic that works on its own. The most consistent results come from combining a few basics and executing them well, such as intercepting disputes early using alerts and network tools, and keeping billing clear so customers recognise charges. When those are in place, representment becomes the exception rather than the default.

Some effects are immediate. Early alerts and automated resolution can reduce chargeback volume in the same billing cycle because disputes are stopped before they escalate.

Other improvements, like cleaner billing or better refund handling, tend to show results over a few weeks as customer behaviour adjusts. Prevention works fastest when you start with the biggest sources of repeat disputes.

Yes, but the focus is different.

Subscription and SaaS chargebacks are often driven by renewals customers didn’t expect or cancellations that didn’t stick. Prevention here focuses less on fraud controls and more on clear sign-up flows, visible billing schedules, renewal reminders, and frictionless cancellation. When those are handled properly, dispute volume drops sharply.