Chargeback Representment: The Complete Guide to Disputing and Winning Chargebacks

Chargebacks don't have to be final. This guide covers how representment works, what evidence wins disputes, and how to recover revenue across all card networks.

Chargeback Representment in 30 Seconds

When a customer files a chargeback, their bank reverses the transaction automatically — often before you even know a dispute has been raised. Representment gives you the formal opportunity to fight back by submitting evidence that proves the transaction was legitimate, the goods were delivered, or the service was rendered as described.

The card network reviews your submission and makes a decision based on the strength of your evidence and how well it aligns with the relevant reason code. A successful representment returns the funds to your account; a failed one means the loss is final, the chargeback stands, and the transaction is recorded against your chargeback ratio.

Dispute and Win More Chargebacks with Strong Chargeback Representment

Chargebacks are one of the most frustrating challenges merchants face. A customer claims they didn't receive their order, didn't recognize the charge, or disputes the quality of service. Within days, your revenue is reversed, and you're left scrambling to recover the lost funds. But here's what many merchants don't realize: you’ve got powerful legal and procedural rights to fight back.

Chargeback representment is your formal opportunity to challenge a chargeback before it becomes final. With the right evidence, a compelling narrative, and clear understanding of the rules, you can recover revenue that seemed lost.

Whether you're new to chargebacks or you've been fighting them for years, this guide will help you understand your options, avoid costly mistakes, and recover more revenue. And if you'd rather have experts handle it for you, ChargebackStop can help manage the entire process.

What Is Chargeback Representment?

Chargeback representment is your formal response to a chargeback; it’s your chance to tell the card network and the issuing bank that the cardholder's claim is wrong. When a customer disputes a transaction, the card network doesn't automatically side with them. Instead, they allow you to represent your side of the story with evidence.

Representment is not the same as simply accepting the chargeback or ignoring it. It's an active, structured process where you submit documentation, a rebuttal letter, and transaction details that prove the cardholder either authorized the transaction or received the goods or services they paid for. If your evidence is compelling enough, the card network or bank will reverse the chargeback and return your funds.

The stakes are high, though. A successful representment keeps revenue in your account, but a failed representment means the chargeback stands, your money is gone, and you may face increasing chargeback ratios that put your merchant account at risk. That's why understanding the process, gathering the right evidence, and making a strong case are extremely important.

Chargeback Representment

Chargeback representment is the formal process of contesting a chargeback by submitting evidence and a rebuttal to the card network through your acquiring bank. If the evidence is compelling enough, the network overturns the dispute and returns the funds to your account.

What's the Difference Between Representment and Recovery?

Chargeback representment vs chargeback recovery are terms often used interchangeably, but they have slightly different meanings.

- Representment is the specific process of submitting evidence and a response to dispute a chargeback within the card network's timeline.

- Recovery is the broader goal: getting your money back through any means, such as representment, settlement negotiations, or arbitration.

In practice, representment is your first and most important tool for recovery. It's the fastest, most direct path to win a chargeback. Chargeback recovery can also happen through other channels, like working directly with your acquirer or pursuing arbitration if representment fails. But representment remains the foundation of any recovery strategy.

When Does Representment Make Sense?

Representment makes sense in most cases, especially when you have strong evidence, but it's not always the right move. You should represent a chargeback if:

- You have proof that the cardholder authorized the transaction (payment confirmation, account login data, delivery confirmation)

- You delivered goods or services as described (shipping receipts, delivery signatures, product images, fulfillment records)

- The transaction matches the reason code dispute (for example, if the claim is unauthorized and you have an AVS match)

- Your overall chargeback ratio is at risk, and fighting helps you reduce it

- The chargeback amount is large enough to justify the effort and cost

In some cases, you should accept the chargeback and move on. If you have no evidence, if the customer clearly has a legitimate dispute, or if the amount is too small to justify your time, accepting may be smarter than fighting a losing battle.

The Representment Window: How Long Do You Have?

Time is critical with representment. Once a chargeback is filed, you’ve got a limited window to submit all your documentation. The timeline varies by card network:

- Visa: You typically have 10 calendar days from the chargeback notification to submit your response.

- Mastercard: You have 7 calendar days to submit a response to Mastercard directly, but your acquirer may have earlier internal deadlines.

- American Express and Discover: Timelines vary but are typically 7 to 14 days.

These windows are non-negotiable, and missing the deadline means an automatic loss. Many merchants don't realize how quickly the clock ticks, especially if the chargeback notification arrives during a weekend or holiday. That's why automated systems and managed services are so valuable; they catch chargebacks immediately and ensure deadlines are never missed.

Understanding the Chargeback Lifecycle

To win at representment, you need to understand the full journey of a chargeback. Each stage has different rules, different evidence requirements, and different opportunities to fight back. Here's how the process works from filing to resolution.

Stage 1: Chargeback Filed

It all starts when a cardholder contacts their bank and disputes a transaction. They might claim they didn't authorize it, didn't receive the goods, or received something different than what they ordered. The bank (the issuing bank) reviews the claim and decides whether to open a chargeback investigation.

At this stage, without pre-chargeback alerts, you typically have no idea a chargeback is coming. The first notification comes from your acquirer (payment processor or merchant bank) via email, dashboard alert, or portal notification. The chargeback notification includes the cardholder's claim, the reason code, the transaction details, and your representment deadline.

As soon as you learn about a chargeback, the clock starts immediately. You now have just days to gather evidence, build your case, and submit your response.

Stage 2: Representment (Your Response)

This is your main opportunity to fight. You submit a formal response packet that includes:

- A rebuttal letter explaining why the cardholder's claim is wrong

- Evidence supporting your position (order confirmations, delivery receipts, communications, etc.)

- Transaction details and merchant documentation

- Any relevant correspondence with the cardholder

The card network or bank reviews your submission and makes a decision. If your evidence is compelling, they reverse the chargeback, and the funds return to your account. If not, the chargeback proceeds to the next stage.

Most chargebacks are resolved at this stage. If you’ve got solid evidence and a well-written rebuttal, you have a strong chance of winning. This is why representment can be your best shot at recovery if managed properly.

Stage 3: Pre-Arbitration

If the issuing bank upholds the chargeback despite your representment, the dispute escalates. Both parties (the cardholder's bank and your acquiring bank) may submit additional evidence and arguments. This is sometimes called the pre-arbitration or appeal stage.

At this level, the card network gets more involved, and they'll review all submitted materials and make a binding decision. The standards are stricter, the evidence requirements more technical, and the process more formal. Many merchants don't pursue this stage because the cost and complexity increase significantly.

Stage 4: Arbitration

If pre-arbitration doesn't resolve the dispute, either party can escalate to arbitration. This is a formal proceeding where both sides present their cases to the card network's arbitration team. Arbitration is expensive, time-consuming, and binding. The card network makes a final decision, and there's no further appeal.

Most merchants and cardholders never reach arbitration because the costs are often extremely high relative to the chargeback amount, and the outcome is uncertain. But for high-value chargebacks or disputes of principle, arbitration may be worth pursuing.

What Happens if You Accept the Chargeback?

If you choose not to represent (or if representment fails), the chargeback becomes final. The funds remain reversed, and the transaction is marked as a loss against your merchant account. You also lose the customer relationship and any product or service they received.

Beyond the immediate financial loss, chargebacks impact your merchant account health. Card networks track your chargeback ratio, which is the percentage of transactions that result in chargebacks.

If your ratio exceeds network thresholds, you may face higher processing fees, mandatory monitoring, or even account termination. That's why it's important to only fight chargebacks when it makes sense to do so, rather than being influenced by an emotional response.

How to Build a Winning Representment Case

Winning a chargeback requires strategy, evidence, and clarity. A compelling rebuttal letter backed by weak evidence will lose. Overwhelming evidence without a clear narrative will lose. You need both. Here's how to build a case that wins.

Gather Your Evidence

Evidence is the foundation of every winning representment. Without it, even a perfect letter won't convince anyone. Here's what you need to collect immediately after learning about a chargeback:

- Transaction details: Order number, transaction ID, amount, date, cardholder name, card last four digits, and authorization code.

- Order information: What was ordered, quantity, description, price, any add-ons or special requests.

- Proof of delivery: Shipping confirmation with tracking number, signature confirmation, carrier receipt, or delivery photo.

- Customer communications: All emails, chat logs, order confirmations, and support tickets related to this transaction.

- Product or service details: If applicable, photos of shipped items, digital delivery records, access logs, or service dates.

- Authorization evidence: AVS match results, CVV match, IP address information, device fingerprinting, or user account history.

- Customer account history: Previous transactions, account age, customer lifetime value, or any pattern of disputes.

The key is to gather evidence immediately, before details fade from memory or records are lost. Many merchants wait to fight a chargeback, only to find that they can't locate critical documentation. Set up systems now to capture and store this data automatically.

Write a Compelling Rebuttal Letter

Your rebuttal letter is your narrative. It connects the evidence to the cardholder's claim and explains why their claim is incorrect. A strong rebuttal letter does three things:

- Addresses the specific reason code and claim directly.

- Tells a clear, logical story that contradicts the cardholder's narrative.

- Points to specific evidence that proves your position.

The tone matters, so be professional, factual, and respectful, and avoid emotional language, accusations, or defensiveness. You're not arguing with the cardholder; you're presenting evidence to an impartial reviewer. Stick to facts, reference your evidence, and let the data speak.

For example, if the claim is 'unauthorized transaction,' your letter should explain:

- How the cardholder authorized it (account login, unique customer identifier.)

- When they authorized it.

- What evidence proves authorization.

- Why the cardholder may be claiming otherwise (forgotten password, family member used card, etc.)

Match Your Response to the Reason Code

Every chargeback comes with a reason code — a standardized code that describes the cardholder's claim. Reason codes vary by card network and define what evidence you need and what your argument should be.

For example, Mastercard Reason Code 4855 is 'Goods and Services Not Provided.' Your response must prove delivery or service completion. 4855 is different from Mastercard Reason Code 4837, 'No Authorization,' which requires proof of authorization instead. Matching your rebuttal and evidence to the specific reason code dramatically improves your chances.

Card networks provide detailed guides on what evidence is required for each reason code. If you're unfamiliar with the codes relevant to your business, take time to learn them; this knowledge alone can improve your win rate by 10-20%.

What is a Reason Code?

Chargeback reason codes are alphanumeric codes that card networks use to categorize disputes. When a chargeback is filed, the issuing bank assigns a code that describes the cardholder's claim. That code dictates the evidence requirements for representment — submit the wrong evidence for the wrong code, and you'll lose regardless of how strong your case appears.

Submit Through the Right Channel

You don't submit representments directly to the card network. Instead, you submit through your acquirer or a representment service. Here's how it typically works:

- Self-service through your processor's portal: Many payment processors (Stripe, Adyen, Authorize.Net) let you submit representments through your merchant dashboard.

- Through your acquiring bank: Contact your acquirer directly for submission instructions.

- Through a representment service provider: Platforms like ChargebackStop, Verifi, or Ethoca offer managed representment services.

Regardless of channel, make sure you submit before the deadline and confirm receipt. Some merchants submit at the last minute and experience delays that cause them to miss the window. Submit early, confirm submission, and track the deadline in your calendar.

Compelling Evidence: The Foundation of Every Win

The card networks have specific standards for what qualifies as 'compelling evidence.' Understanding these standards is essential because evidence that seems compelling to you might not meet the card network's technical requirements. Let's break down what actually works.

What is Compelling Evidence?

Compelling evidence is documentation that directly contradicts the cardholder's claim and comes from a reliable source. It must be:

- Original and unaltered: Screenshots, photos, or documents must be genuine and unmodified.

- Specific to the transaction: Generic policies or standard terms don't count. Evidence must relate directly to this cardholder, this transaction, this order.

- Contemporaneous: Documentation created around the time of the transaction is more credible than documentation created months later.

- Third-party verified: Evidence from independent sources (payment processors, shipping carriers, delivery services) carries more weight than internal records alone.

- Technical or system-based: Data from your systems (IP logs, device fingerprints, login records) proves cardholder behavior better than subjective claims.

Not all evidence carries equal weight. A shipping receipt from a major carrier (FedEx, UPS, USPS) is more compelling than an internal shipping log. Similarly, a payment processor's authorization record is more compelling than a screenshot of your own system. Keep this hierarchy in mind when gathering evidence.

Visa Compelling Evidence 3.0 (CE3.0)

Visa's Compelling Evidence 3.0 framework sets specific standards for what evidence wins chargebacks in their network. Understanding CE3.0 is therefore crucial if you process Visa transactions.

CE3.0 defines different evidence categories based on the type of service or product sold and the reason code. For example, for goods shipped with tracking, CE3.0 requires a tracking number from a major carrier and delivery confirmation. For digital goods, it requires access logs or IP address information. For services, it requires appointment details, payment authorization records, or service dates.

Visa publishes the full CE3.0 framework publicly. If you're handling Visa chargebacks regularly, download and study it. Submitting evidence that aligns with CE3.0 standards dramatically increases win rates. Evidence that doesn't fit the framework, no matter how convincing, won't work.

Representment Win Rates

What's a realistic win rate for chargebacks? The answer depends on your evidence quality, your rebuttal strategy, and your business model. But industry benchmarks can help set expectations.

Industry Benchmarks

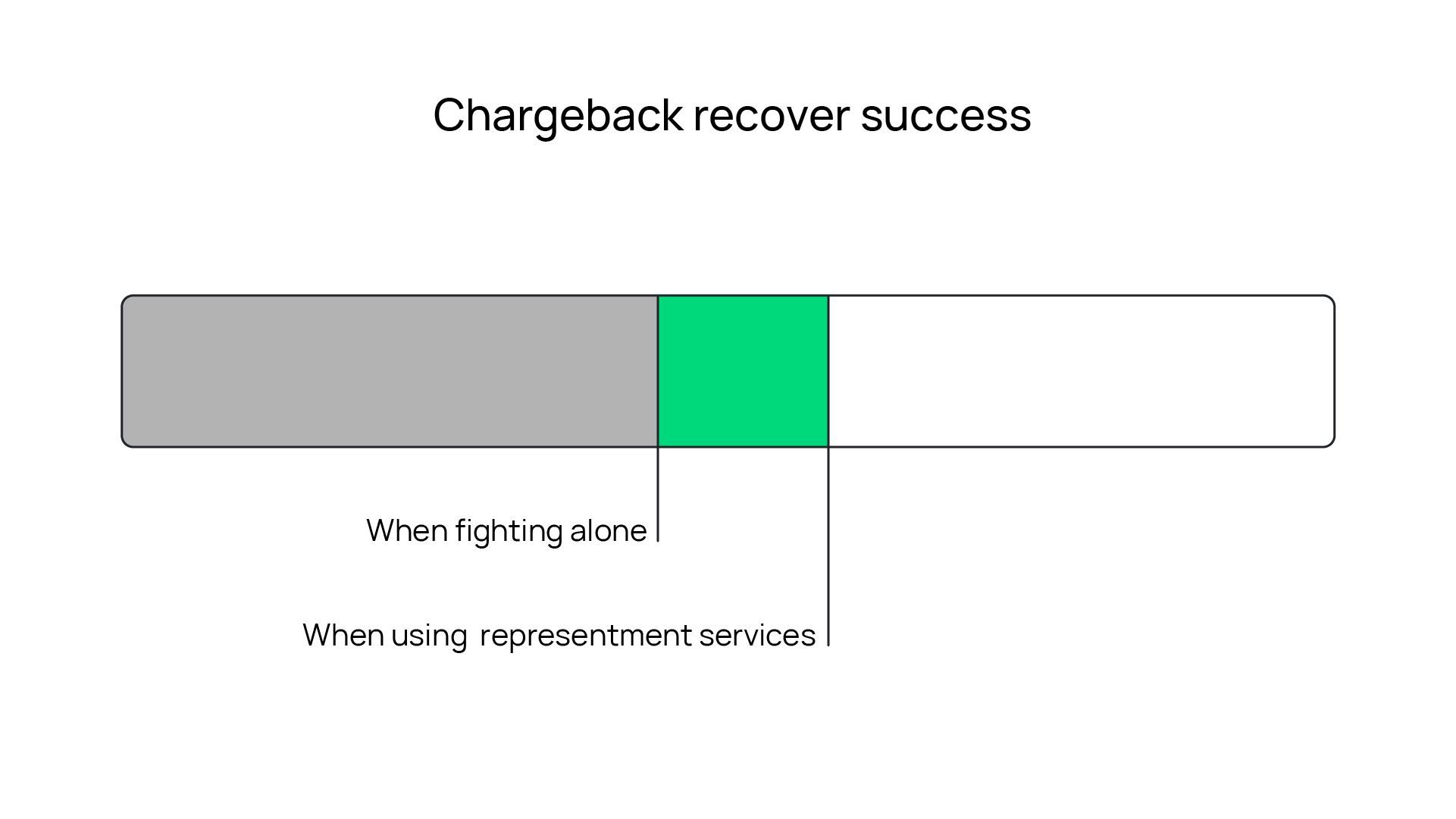

Research and industry reports suggest that merchants fighting chargebacks themselves win approximately 35-45% of the time. This means for every 100 chargebacks you challenge, you successfully recover 35-45. The rest are lost despite your effort.

Why is the win rate so low? Because most merchants lack sophisticated evidence collection systems, miss critical documentation, or submit incomplete or poorly written rebuttals. Many merchants also don't understand reason codes deeply, so they submit evidence that doesn't match the card network's specific requirements for that dispute type.

In contrast, merchants using managed representment services report win rates of 40-60%, sometimes higher. These services have processes, templates, and expertise designed to maximize evidence quality and argument clarity. ChargebackStop's managed representment service, for example, helps merchants exceed the 35-45% baseline by handling evidence collection, rebuttal writing, and submission professionally.

Why Most Representments Fail

Understanding why representments fail is as important as understanding how to win. Here are the most common reasons chargebacks go against you:

- Missing evidence: You submitted a rebuttal but no tracking confirmation, delivery photo, or authorization proof. Without specific evidence, the card network defaults to siding with the cardholder.

- Evidence doesn't match reason code: You submitted delivery confirmation for a 'not as described' dispute, but CE3.0 requires product photos and specifications instead.

- Weak or unclear rebuttal: Your letter is vague, emotional, or fails to directly address the cardholder's claim. Reviewers can't connect the dots.

- Missed deadline: You submitted after the representment window closed. Automatic loss.

- Expired or partial documentation: You submitted a screenshot from your system, but the card network requires official documentation from a third party (carrier, payment processor, etc.).

- No response to customer contact: If the cardholder contacted customer service and you didn't respond appropriately, that history can work against you.

- Pattern of complaints: If the customer has previous chargebacks or complaints, the card network may assume a pattern of fraud.

The good news is that most of these failures are preventable. Stronger systems, earlier evidence collection, and knowledge of reason codes can flip losses to wins.

7 Tips to Help Improve Your Representment Win Rate

- Automate evidence collection: Capture shipping confirmations, delivery photos, authorization records, and customer communications automatically and store them immediately. Don't rely on manual collection later.

- Study reason codes: Download the Visa CE3.0 framework and Mastercard's chargeback guides. Understand which evidence categories matter for which codes. This alone can improve your win rate by 10-15%.

- Create rebuttal templates: Build templates for the most common reason codes you face. Templates ensure consistency, compliance, and clarity. They also save time.

- Use third-party verification: Whenever possible, include evidence from independent sources (carriers, payment processors, services platforms). This evidence is weighted more heavily than internal records.

- Train your support team: Ensure customer service staff understand the chargeback process. When customers contact support with complaints, staff should document everything thoroughly.

- Implement payment authentication: Use 3D Secure, EMV, or other authentication methods. These create stronger authorization proof and reduce both chargebacks and representment battles.

- Consider a managed service: If you're handling representments internally and losing frequently, a managed service may be worth the investment. The improved win rate quickly offsets the service cost.

When NOT to Fight a Chargeback

Not every chargeback is worth fighting. Sometimes accepting the loss is the smarter business decision, and knowing when to walk away is just as important as knowing when to push back.

The most obvious case is when you simply have no evidence. Without shipping confirmation, authorization records, or delivery proof, you'll lose the representment — and the time spent building a losing case costs more than the chargeback itself. The same logic applies when the customer has a legitimate grievance. If they genuinely received damaged goods, poor service, or something materially different from what you advertised, contesting the dispute is both futile and ethically difficult to justify.

Dollar value matters too. If the disputed amount is $10–$15, even 30 minutes of staff time to contest it exceeds what you'd recover. Accept it and move on. A similar calculation applies if you're dealing with a known problem customer, such as someone with multiple disputes or complaints on record. Blacklist them, absorb the loss, and redirect your energy elsewhere.

Your chargeback ratio should also factor into the decision. If you're comfortably below network thresholds — say, well under 0.5% — fighting every minor dispute adds operational overhead without improving your standing.

What is a Chargeback Ratio?

Card networks and acquirers don’t just care how many chargebacks you have. They care about how many you have relative to your successful transactions. That percentage is your chargeback ratio, and it carries more weight in their decision-making than any individual dispute.

Prioritize high-value cases or disputes that suggest a fraud pattern worth investigating. Conversely, if your ratio is critically high and account termination is a real risk, the priority shifts entirely. Accepting smaller losses and focusing on prevention will do more for your processing health than contesting chargebacks you're unlikely to win.

Being selective about which disputes you fight preserves resources for the cases where you have a genuine shot, and where the outcome actually has an impact

Automate Representment with ChargebackStop

The most common barrier to winning chargebacks is time. Gathering evidence, writing rebuttals, and managing submissions is work — work that most merchants don't have bandwidth to do well. That's where ChargebackStop comes in.

ChargebackStop's platform offers two approaches to representment: self-service and managed.

With the self-service option, you use ChargebackStop's guided workflows and templates to build your own representments. The platform handles evidence organization, provides reason-code-specific templates, tracks deadlines, and manages submission through Visa (Verifi) and Mastercard (Ethoca) networks. This puts the control in your hands while automating the administrative burden.

With the managed representment service, ChargebackStop's team takes over. We handle evidence collection from your systems, interview you about the transaction, write the rebuttal letter, organize the evidence packet, and submit it before the deadline. Our team brings expertise in reason codes, card network standards, and winning arguments. Merchants using ChargebackStop's managed service see win rates 35-45% higher than their DIY baseline.

ChargebackStop also integrates with major payment processors (Stripe, Adyen, Authorize.Net, Shopify) and card networks (Verifi for Visa, Ethoca for Mastercard). This integration means chargebacks are captured automatically, evidence is pulled from your sales records automatically, and timelines are managed automatically.

For merchants processing thousands of transactions monthly, this automation prevents chargebacks from falling through the cracks. For merchants with high chargeback volume, it transforms representment from a chaotic scramble to a structured, winnable process.

Ready to Win More Chargebacks?

Chargeback representment is complex, time-consuming, and critical to your business. You need systems, evidence, expertise, and speed. Doing it well matters.

Whether you represent chargebacks yourself or work with a service, the principles in this guide apply. Gather evidence early, understand reason codes deeply, match your rebuttal to the specific dispute, and meet your deadlines. These fundamentals drive wins.

Want to stop fighting chargebacks alone? ChargebackStop's managed representment service handles evidence collection, rebuttal writing, and submission, so you recover more revenue with less effort. Our merchants see win rates 35-45% higher than DIY efforts.

Win more chargebacks without the paperwork

Our managed representment service handles evidence collection, rebuttal writing, and submission for you. See how much revenue you could recover.

Chargeback Representment FAQs

Straight answers to the questions merchants actually ask about chargeback representment.

The representment process typically takes 30-75 days from submission to final decision. Visa and Mastercard have different timelines, and issuers may take additional time to investigate. You'll receive notification once a decision is made. ChargebackStop tracks timelines and notifies you of any delays.

No. The representment deadline is firm and non-negotiable. Missing it results in an automatic loss. That's why automated tracking and managed services are so valuable; they ensure deadlines are never missed.

Not for self-service representment through most payment processors. However, managed representment services typically charge a fee (often a percentage of the chargeback amount or a flat fee). The fee is usually worth the improved win rate, but compare the cost to your expected recovery before committing.

The chargeback becomes final, the funds remain reversed, and the transaction is recorded against your chargeback ratio. If you lose, you may pursue pre-arbitration or arbitration, but this is more complex and costly. Some merchants simply accept losses they determine aren't worth fighting further.

Yes, if the chargebacks are identical (same cardholder, same transaction, same reason code). However, each chargeback is reviewed separately. If you have multiple disputes from different customers or for different transactions, each requires its own representment with transaction-specific evidence.