Chargeback Monitoring Programs: Thresholds, Fines, and How To Stay Out of Them

Learn how chargeback monitoring programs work, what triggers enrollment, and how to keep your ratio well below network thresholds.

Chargeback Monitoring Programs in 30 Seconds

Chargeback monitoring programs are initiatives run by Visa and Mastercard to identify merchants generating excessive dispute volumes. When your chargeback ratio crosses the relevant threshold, you're enrolled automatically, triggering monthly fines, mandatory reporting, and oversight from your acquiring bank.

Each network runs its own program with its own thresholds and remediation requirements. Visa's program is VAMP, which monitors a combined ratio of fraud and non-fraud disputes. Mastercard operates the Excessive Chargeback Merchant (ECM) program, which tracks chargebacks as a percentage of total transactions. Both give merchants a defined window to remediate, and both escalate to account termination if they don't.

Top topics in Chargeback Monitoring Programs

Merchants' Guide to Chargeback Monitoring Programs

Chargebacks are an inevitability for merchants. But what happens when chargebacks become too frequent? Card networks like Visa and Mastercard have implemented monitoring programs designed to protect both themselves and honest merchants from excessive chargeback activity. If your chargeback ratio climbs too high, you could face enrollment in one of these programs, triggering fines, enhanced oversight, and the risk of account termination.

This guide walks you through everything merchants need to know about chargeback monitoring programs in 2026. We'll explain what these programs are, how they work, what thresholds trigger enrollment, what penalties you'll face if enrolled, and most importantly, how to stay out of them entirely.

What Are Chargeback Monitoring Programs?

Chargeback monitoring programs are initiatives established by Visa, Mastercard, and other card networks to identify and remediate merchants with excessive chargeback activity. These programs exist for a simple reason: chargebacks are expensive for the networks, issuing banks, and the wider payments ecosystem. When a merchant generates too many chargebacks, it signals either poor business practices, inadequate fraud prevention, or both.

A monitoring program enrollment is essentially a warning system with teeth. Once enrolled, merchants face increased scrutiny, monthly fines, mandatory reporting requirements, and the constant threat of account suspension or termination if they don't improve. The goal isn't to punish merchants, but to incentivize them to reduce chargeback volume and improve their operational and fraud prevention practices.

Chargeback Monitoring Thresholds

Chargeback monitoring thresholds are the ratio limits card networks use to identify merchants generating excessive dispute volume. When your chargeback rate crosses those limits, Visa or Mastercard enrolls you in a monitoring program. Enrolled merchants face escalating monthly fines, mandatory reporting to their acquirer, and a defined window to demonstrate improvement. Fail to bring the ratio down in time, and the network can move toward account suspension or termination.

Why Card Networks Created Monitoring Programs

Before monitoring programs existed, merchants with chronically high chargeback rates could continue operating indefinitely, generating losses for the networks without meaningful consequences. Visa and Mastercard created these programs to shift financial and operational responsibility back to merchants, who are in the best position to prevent fraud and disputes at the source.

From the networks' perspective, a merchant with a 2% chargeback ratio is a liability. Each chargeback costs the network time, money, and reputation. Issuing banks and acquiring banks share these costs. The networks also face regulatory scrutiny if chargeback rates grow too high because it signals systemic problems in the payments ecosystem. Monitoring programs help the networks maintain control and ensure that merchants take fraud prevention and customer service seriously.

For merchants, the existence of these programs should be a wake-up call: your chargeback ratio directly impacts your ability to accept payment cards. High ratios can be financially devastating and operationally disruptive.

Disputes vs Fraud: Two Different Metrics

It's critical to understand the distinction between disputes and fraud when discussing monitoring programs. These two categories are tracked separately because they reflect different problems.

A dispute is a chargeback filed by a customer who claims they didn't authorize a transaction, don't recognize it, or received defective goods or services. Disputes are often rooted in customer service issues, unclear billing descriptors, or legitimate product problems. A fraud chargeback is filed when a customer's card was used without their permission, typically due to card theft, account compromise, or CNP (card-not-present) fraud.

Both metrics are measured as ratios — chargebacks divided by transaction volume — and both have separate thresholds in monitoring programs. Understanding which type of chargeback is dragging down your ratio helps you focus your remediation efforts. If your dispute ratio is high, you might need better customer service or clearer billing practices. If your fraud ratio is high, you need stronger fraud detection and prevention tools.

Who Gets Enrolled, and How?

Enrollment in a monitoring program is automatic and mandatory for merchants whose thresholds are out of control. Visa and Mastercard monitor all merchant activity on their networks continuously, and when a merchant's ratio crosses the threshold for their program level, the acquirer (the bank that processes payment cards for the merchant) receives notification. The merchant is then notified that they're enrolled and must comply with program requirements.

The process is straightforward but the consequences are not. Once enrolled, you'll typically receive a formal notice from your acquiring bank detailing your enrollment tier, your current ratio, the required remediation plan, monthly fines, and the date by which you must drop below the threshold to exit the program. There's no appeal process — the only way out is to improve.

Visa's Chargeback Monitoring Program

Visa manages one of the largest payment card networks in the world, which means it processes billions of transactions annually. In response to monitoring needs, Visa has evolved its monitoring frameworks significantly, and in 2025 transitioned to the unified Visa Acquirer Monitoring Program (VAMP).

VAMP launched in April 2025 as Visa's consolidated approach to monitoring merchant chargebacks and fraud. This program replaces two previous frameworks: the Visa Dispute Monitoring Program (VDMP) and the Visa Fraud Monitoring Program (VFMP). By unifying these programs, Visa aims to streamline merchant oversight and provide a clearer, more transparent path for merchants to understand their standing on the network.

VAMP operates on a tiered system with separate thresholds for dispute and fraud activity. Unlike the previous programs, which had distinct operational requirements, VAMP brings both metrics under one umbrella, making it easier for merchants to track their exposure and easier for acquirers to enforce compliance. The program includes monthly monitoring, automated notifications, and a clear escalation path if merchants fail to remediate within required timeframes.

The previous VDMP focused exclusively on excessive dispute chargebacks filed by customers claiming they didn't authorize a transaction or didn't receive goods or services. VFMP, by contrast, focused on fraud chargebacks where the customer's card was used without authorization. The two programs had different thresholds, different timelines, and different remediation requirements, which created confusion for merchants managing multiple metrics simultaneously.

VAMP consolidates this framework. Under VAMP, merchants are monitored against both dispute and fraud thresholds simultaneously, with clear escalation tiers for each. This means merchants can see exactly where they stand on both metrics and understand which specific area (disputes or fraud) is driving their risk. The unified approach also simplifies acquirer compliance and makes the monitoring criteria more transparent to merchants.

VAMP Dispute Ratio Thresholds: Standard vs. Excessive

VAMP uses a tiered threshold system for disputes. Under Visa's current guidelines, merchants are monitored against two primary dispute ratio thresholds.

The Standard tier threshold is approximately 0.9% dispute ratio. Merchants at or above 0.9% are flagged as having elevated dispute activity and may face increased monitoring, reporting requirements, and minor fines. The Excessive tier threshold is approximately 1.8% dispute ratio. Merchants crossing this threshold are subject to significantly higher fines, mandatory remediation plans, and enhanced oversight.

It's important to note that these thresholds may vary slightly by acquirer and are subject to change. Merchants should verify exact thresholds with their acquiring bank. Additionally, transaction volume is important because a small merchant with 1,000 transactions per month will be monitored differently than a large enterprise processing millions of transactions. Visa and most acquirers apply a minimum transaction volume threshold (often 100+ transactions per month) before monitoring begins.

Separate from the dispute ratio, VAMP also monitors for enumeration attacks: automated card testing attempts where fraudsters cycle through large volumes of card numbers to identify valid combinations. The enumeration ratio is calculated by dividing enumerated authorization transactions (both approved and declined) by total authorization transactions, with merchants flagged once that ratio reaches or exceeds 20%.

A minimum of 300,000 enumerated transactions per month must be recorded before the threshold applies. Enumeration exposure is particularly relevant for merchants processing high authorization volumes, and unlike dispute ratios, it can't be remediated after the fact; the only effective response is detection before transactions are authorized.

VAMP Fines and Consequences

VAMP applies a single fine level for merchants: once you're classified as Excessive, you're subject to a fee of $8 per dispute for both fraud and non-fraud instances alike. There's no lower "Standard" tier with reduced fines at the merchant level; that tiered structure applies to acquirers, not merchants. You're either below the threshold or you're not.

Unfortunately, that means financial exposure scales quickly with volume. A merchant processing 10,000 transactions per month at a 2.3% VAMP ratio — just above the current Excessive threshold — is looking at roughly 230 disputes per month, which translates to $1,840 in monthly fines before accounting for the operational cost of managing those disputes. At higher volumes, the monthly liability becomes significant in a short period.

Beyond the per-dispute fines, merchants classified as Excessive face mandatory remediation requirements through their acquirer, and sustained non-compliance can ultimately result in loss of the ability to accept Visa payments. Visa transactions account for close to 40% of global card payments, making that a material business risk.

Mastercard's Chargeback Monitoring Program

Mastercard, the world's second-largest payment card network, operates a similarly stringent but distinct monitoring framework. Mastercard's approach is built around two primary programs: Excessive Chargeback Merchant (ECM) and High Excessive Chargeback Merchant (HECM). These programs are designed to identify and remediate merchants whose chargeback activity exceeds acceptable thresholds.

The Excessive Chargeback Merchant (ECM) Program

Mastercard's ECM program is the entry point for merchant monitoring. Under this program, merchants are flagged when their chargeback activity crosses predefined thresholds. Enrollment in ECM is automatic when Mastercard's monitoring systems detect a violation.

Merchants enrolled in ECM face increased scrutiny from both Mastercard and their acquiring bank. They're required to submit remediation plans, implement specific fraud prevention measures, and maintain detailed reporting on their chargeback reduction efforts. The program also carries fines of $5–$10 per chargeback in the monitoring period, assessed monthly.

The High Excessive Chargeback Merchant (HECM) Program

HECM is Mastercard's escalated program for merchants with the most severe chargeback problems. Enrollment in HECM indicates that a merchant has failed to remediate under ECM or has rates so high that they bypass ECM entirely and go straight to HECM. HECM merchants face substantially higher fines, mandatory fraud prevention technology implementation, weekly reporting, and a significantly elevated risk of account termination.

Merchants in HECM typically have 30–60 days to reduce their chargeback ratio below the HECM threshold or face account suspension. That's a real threat and isfrequently executed, and many acquiring banks will not continue processing for merchants in HECM beyond a short grace period.

ECM and HECM Thresholds

Mastercard's ECM program is triggered when a merchant reaches a 1.5% chargeback rate, with a minimum transaction volume threshold of 100 chargebacks per month. This means a merchant needs both a high ratio and significant volume before triggering ECM — a small merchant with 5 chargebacks in a month wouldn't be enrolled, even if those chargebacks represented a 10% ratio.

HECM is triggered at a 3.0% chargeback rate (monthly), also with minimum volume requirements. Additionally, Mastercard has absolute volume thresholds meaning, for example, merchants with 100+ chargebacks in a single month may be flagged even if their ratio is below 3.0%, because the absolute volume suggests systemic problems.

These thresholds apply across all merchant categories unless Mastercard has granted specific exemptions for high-risk verticals.

Mastercard's Fines and Remediation Requirements

ECM fines typically start at $5–$10 per chargeback, assessed monthly. For a merchant at 1.5% ratio processing 10,000 monthly transactions (150 chargebacks), fines would run $750–$1,500 per month. HECM fines are substantially higher, often $25–$50 per chargeback or more, depending on the acquiring bank's policies.

Beyond fines, Mastercard requires ECM and HECM merchants to implement specific fraud prevention controls. These typically include Address Verification Service (AVS), CVV verification, 3D Secure (3DS), or advanced fraud detection tools. Merchants must also maintain detailed chargeback logs, submit monthly remediation reports, and attend mandatory compliance meetings with their acquiring bank.

Failure to meet remediation timelines results in account termination, and Mastercard doesn't provide indefinite grace periods. Merchants in HECM who don't reduce their chargeback rate within 60–90 days can lose their merchant account entirely, making it extremely difficult to accept Mastercard or any payment cards in the future.

The MATCH List: Mastercard's Terminated Merchant File

Beyond ECM and HECM, Mastercard maintains the MATCH list (Member Alert To Control High-risk merchants).

The MATCH list is Mastercard's network-wide blacklist of terminated merchants. Once your merchant account is terminated due to chargeback violations (or other compliance failures), you're added to MATCH. Being on MATCH makes it nearly impossible to open new merchant accounts across the Mastercard network, and it can severely limit your ability to accept payment cards from other networks as well.

What Gets You on MATCH

Merchants are added to MATCH for various violations, but chargeback-related terminations are among the most common. Specific triggers include:

- Failure to remediate chargebacks while in ECM or HECM (exceeding the grace period)

- Chargebacks exceeding 4–5% of transaction volume for extended periods

- Intentional or repeated violation of Mastercard's fraud prevention requirements

- Criminal activity, fraud, or deliberate chargebacks filed by the merchant

- Failure to maintain minimum processing volume or account activity

Once added to MATCH, you remain on the list for five years. During that time, acquiring banks will deny your merchant account applications automatically, because MATCH is a compliance checkpoint for all acquiring banks. Some banks may consider applications after three years with documented improvement, but most won't. The five-year period is Mastercard's way of ensuring that merchants learn their lesson and implement lasting changes.

How to Get off MATCH

There is no formal removal process for MATCH — you age off after five years. However, in rare cases, Mastercard may remove merchants earlier if they can demonstrate extraordinary remediation efforts. This requires submitting a formal appeal to Mastercard with documented evidence of fraud prevention implementation, chargeback reduction (often requiring complete account closure and restart), third-party audits, and sometimes legal counsel involved in the process.

For practical purposes, merchants should treat MATCH as a permanent consequence of account termination. The better strategy is never to reach that point. By staying vigilant about chargeback ratios, implementing fraud prevention tools proactively, and addressing disputes early, merchants can avoid the MATCH list entirely.

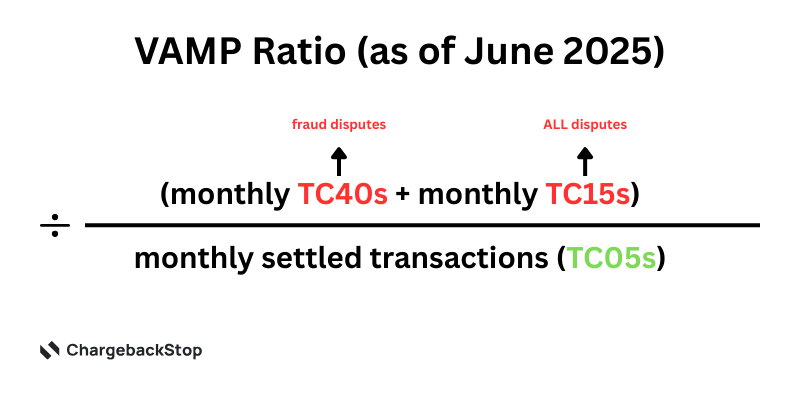

How Are Chargeback Ratios Calculated?

Chargeback ratio is calculated as: (Total Chargebacks in Period) ÷ (Total Transaction Count in Period) = Chargeback Ratio.

For example, if you process 100,000 transactions in a month and receive 1,500 chargebacks, your chargeback ratio is 1,500 ÷ 100,000 = 0.015 or 1.5%. This straightforward formula applies to both Visa and Mastercard, and both dispute and fraud ratios use the same calculation method.

Most monitoring programs assess ratios on a monthly basis, so your ratio is recalculated each month based on transactions and chargebacks from that specific calendar month. Some programs look at rolling 12-month averages for certain assessments, but monthly is the standard. This means a single bad month can trigger enrollment, even if your annual average is within acceptable ranges.

Visa vs. Mastercard Calculation Differences

While the basic formula is identical, Visa and Mastercard differ in how they define transaction volume. Visa typically counts all transaction attempts, including declined transactions, in the denominator. Mastercard's definition can vary slightly, but generally follows a similar approach. This difference rarely impacts small merchants but can create variance for large volume merchants processing millions of transactions.

Additionally, Visa and Mastercard differ in which chargebacks are included. Both programs exclude certain chargeback types (such as fraud chargebacks from stolen cards reported before the transaction) from ratio calculations in specific circumstances. These exclusions are rare and highly dependent on the merchant's fraud prevention practices and documentation. Merchants should consult their acquirer for exact calculation methodology applicable to their account.

Common Calculation Mistakes

The most common mistake merchants make is misidentifying their transaction volume. Many merchants look at sales volume (gross revenue) rather than transaction count. These are entirely different metrics. A merchant selling high-ticket items might have fewer transactions but similar revenue to a merchant selling low-ticket items. Chargebacks are calculated on transaction count, not dollars.

Another mistake is failing to distinguish between chargebacks filed and chargebacks lost. Only chargebacks that result in money being reversed to the customer (i.e., chargebacks you didn't successfully dispute) count toward your ratio. If you fought back with representment and won, that chargeback still counts in the ratio denominator, but your successful defense reduces the actual financial impact. This is an important distinction because your ratio is a percentage of all disputes, not just the ones you lost.

Finally, merchants sometimes conflate disputes filed with chargebacks received. Not all customer disputes result in chargebacks. Some are resolved before chargeback filing. However, chargebacks received are what matters for monitoring; your ratio is based on actual chargeback filings by issuing banks, not customer complaints.

What Are the Consequences of Being In a Monitoring Program?

Enrollment in a monitoring program isn't just a financial hit, but an operational and reputational headache that affects every aspect of your payments infrastructure and business.

Fines and Financial Penalties

As discussed, fines start at $8 per chargeback in the standard tier and escalate rapidly. For a mid-size e-commerce merchant processing 500,000 transactions annually at a 1.5% chargeback ratio, that's 7,500 chargebacks per year x $8 per chargeback = $60,000 in annual fines. This is on top of the operational costs of disputing those chargebacks and the lost revenue from the chargebacks themselves.

These fines are non-negotiable and continue every month until your ratio drops below the threshold. There's no appeal process; the networks calculate your ratio monthly and charge fines accordingly. Fines are typically deducted automatically from your merchant reserve or settlement.

Enhanced Monitoring and Reporting Requirements

Enrollment mandates increased reporting overhead. Standard-tier merchants typically must submit monthly chargeback reports to their acquiring bank detailing remediation efforts. Excessive-tier merchants may face weekly or daily reporting. Some acquiring banks implement automated daily monitoring and require merchants to be available for immediate follow-up if ratios spike.

This reporting burden diverts resources from business operations. If you're a small company with limited compliance staff, you may need to hire personnel specifically to manage chargeback reporting and remediation documentation. Larger enterprises already have compliance teams, but they'll need to shift focus and resources to managing their chargeback liability.

Account Suspension and Termination Risk

The most severe consequence is account termination. If you fail to remediate within the grace period (typically 60–90 days), your acquiring bank will terminate your merchant account. You'll no longer be able to accept Visa, Mastercard, or potentially any payment cards. This is a business-ending event for any company that relies on card payments.

Beyond the immediate impact, termination places you on the MATCH list (if it's Mastercard-related), making it nearly impossible to reopen a merchant account within five years. Even banks and processors from different networks will view a MATCH listing or recent termination as a major red flag and will likely deny your application.

How to Stay Out of Monitoring Programs

The best defense against monitoring programs is prevention. Staying below the thresholds is far easier than trying to remediate once you're enrolled.

Prevention First: Attack Dispute Volume

The largest source of chargebacks for most merchants is customer disputes, such as claims of unauthorized transactions or unmet expectations. These are often preventable through operational improvements. Start by examining your top chargeback reason codes. Are customers claiming they didn't recognize your billing descriptor? Update it to be crystal clear. Are they claiming they didn't authorize the transaction? Implement clearer pre-transaction confirmation.

For subscription merchants, disputes spike when customers forget they've subscribed and see a recurring charge. Implement renewal email reminders and one-click cancellation. For digital goods merchants, disputes happen when customers expect an immediate download that doesn't materialize. Improve your delivery process and customer communication.

Customer service improvements often have a bigger impact on chargeback reduction than technology. A merchant with responsive, helpful customer service can resolve disputes before they escalate to chargebacks. If a customer has a problem and can easily reach your support team, they're far more likely to request a refund than file a chargeback.

Fight Recoverable Chargebacks

Not every chargeback is unrecoverable. For customer disputes about unauthorized transactions or unmet expectations, merchants can file representment, which is a formal response challenging the chargeback with documentation. If a customer claims they didn't authorize a purchase but you have a signed order, shipping confirmation, and IP logs confirming their location, you have a strong representment case.

Many merchants don't fight chargebacks because the process seems complex. But representment is straightforward: you submit evidence within the network's timeframe, the issuing bank reviews it, and makes a final determination. Studies show that merchants with strong representment processes recover 40–60% of representable chargebacks. That directly reduces your overall chargeback count and ratio.

Managed representment services (like those provided by ChargebackStop) make this process easier by handling evidence collection, submission timing, and follow-up automatically. When representment is professional and systematic, recovery rates improve even further.

Monitor Your Ratio Proactively

Don't wait for your acquiring bank to notify you of enrollment. Calculate your own chargeback ratio monthly and trend it over time. Set internal thresholds well below the network limits—aim for 0.3–0.5% dispute ratio and 0.2–0.3% fraud ratio. This gives you early warning if your chargeback activity is trending upward.

Most payment processors now offer chargeback analytics dashboards that show your ratio in real time. If you see your ratio approaching 0.7%, you have time to implement remediation before hitting the 0.9% threshold. But if you're not monitoring, you might cross the threshold before you even realize there's a problem.

How to Exit a Monitoring Program

If you're already enrolled in a monitoring program, exit is possible but requires disciplined action. The timeline depends on how far above the threshold you are and how aggressively you remediate.

- Request a detailed remediation plan from your acquiring bank. This plan outlines specific steps you must take (fraud prevention technology, process improvements, staffing changes) and the timeline for reducing your ratio. Commit to this plan and assign clear ownership.

- Implement aggressive dispute resolution processes. This might include hiring a dispute management specialist, deploying representment software, or partnering with a managed service provider. The goal is to fight every representable chargeback and reduce the denominator (transaction volume) if necessary by exiting high-risk sales channels.

- Identify your largest chargeback drivers and eliminate them. If 40% of your chargebacks come from one product or customer segment, consider discontinuing that offering or implementing stricter controls for that segment. A temporary revenue reduction beats account termination.

Exit timeline typically ranges from 60–180 days. Some merchants drop below thresholds within 60 days with aggressive action, but others require four to six months. The networks want to see sustained improvement; a single good month isn't enough. You'll typically need to stay below the threshold for two to three consecutive months before formal enrollment is lifted.

How ChargebackStop Helps Merchants Stay Compliant

ChargebackStop is built specifically to help merchants reduce chargebacks and stay out of monitoring programs. Here's how our platform works for you:

- Real-time Dispute Prevention: We've integrated Ethoca Alerts and Verifi RDR (Rapid Dispute Resolution) directly into our platform. These tools alert you to potential disputes before they become chargebacks, allowing you to contact the customer and resolve the issue proactively. This prevents chargebacks from being filed in the first place—the most effective way to reduce your ratio. Our merchants prevent over 300,000 chargebacks annually through pre-chargeback intervention.

- Managed Representment & Dispute Recovery: When disputes are filed, ChargebackStop's representment team handles the entire response process. We collect evidence, submit responses within network timelines, and push back on invalid chargebacks. Our 95%+ recovery rate means chargebacks you would have lost often come back as wins, reducing your net chargeback count and ratio impact.

- Real-time Analytics & Ratio Monitoring: Our dashboard shows your current chargeback ratio, dispute vs. fraud breakdown, top reason codes, and trend analysis. You'll see your ratio approaching thresholds before your acquiring bank does, giving you time to act.

- Fraud Pattern Detection: Our TC40 and SAFE fraud notification integration catches fraud patterns early, before they spike your fraud ratio. By identifying compromised accounts and fraud networks quickly, you prevent fraud chargebacks before they occur.

- Compliance Reporting & Documentation: We generate all the reports you need for your acquiring bank and monitoring program compliance, reducing your administrative burden.

The outcome? Merchants using ChargebackStop typically see 30–50% reductions in their chargeback ratio within 90 days. That's the difference between enrollment and staying compliant.

Prevent the disputes that drive up your ratios

ChargebackStop helps you reduce disputes before they're filed, and stay well clear of monitoring programs. See coverage and estimate savings in one call.

Chargeback Monitoring Programs FAQs

Straight answers to the questions merchants actually ask about chargeback monitoring programs.

No. Thresholds are set by Visa and Mastercard and applied consistently across all merchants by all acquiring banks. Your acquiring bank cannot lower the thresholds for you, nor can it exempt you. The thresholds are non-negotiable. However, your acquiring bank can help you develop a remediation plan to stay below them.

Typically 60–180 days, depending on how far above the threshold you are and how aggressively you remediate. The networks want to see sustained improvement, usually across two to three months below the threshold, before officially removing you from the program. Some merchants exit in 60 days; others take six months.

You cannot open new merchant accounts on the Mastercard network. Most acquiring banks and payment processors will deny your application automatically if you're on MATCH. You remain on the list for five years, though early removal is theoretically possible with extraordinary remediation efforts. After five years, you age off automatically and can reapply.

No. Your ratio is based on chargeback filings by issuing banks, not customer refunds you issue directly. If a customer requests a refund and you issue it before a chargeback is filed, it doesn't count against your ratio. This is why pre-chargeback intervention (like Ethoca Alerts) is so effective; it allows you to resolve the issue with a refund before a chargeback is filed.

Technically, yes, but it's not a good strategy. If you have 1.5% ratio on 10,000 transactions, you could reduce volume to 5,000 transactions and maintain 1.5% ratio. However, this cuts your revenue significantly, and the networks are aware of this strategy.

Additionally, monitoring programs often have absolute chargeback volume thresholds (e.g., 100+ chargebacks per month), so reducing volume only helps if you can drop below those thresholds entirely. The better approach is to reduce chargebacks while maintaining volume.