Chargeback Alerts & Prevention Tools: A Complete Merchant Guide

Learn how to stop disputes becoming chargebacks with powerful, easy-to-use alert tools.

Chargeback Alert Tools in 30 Seconds

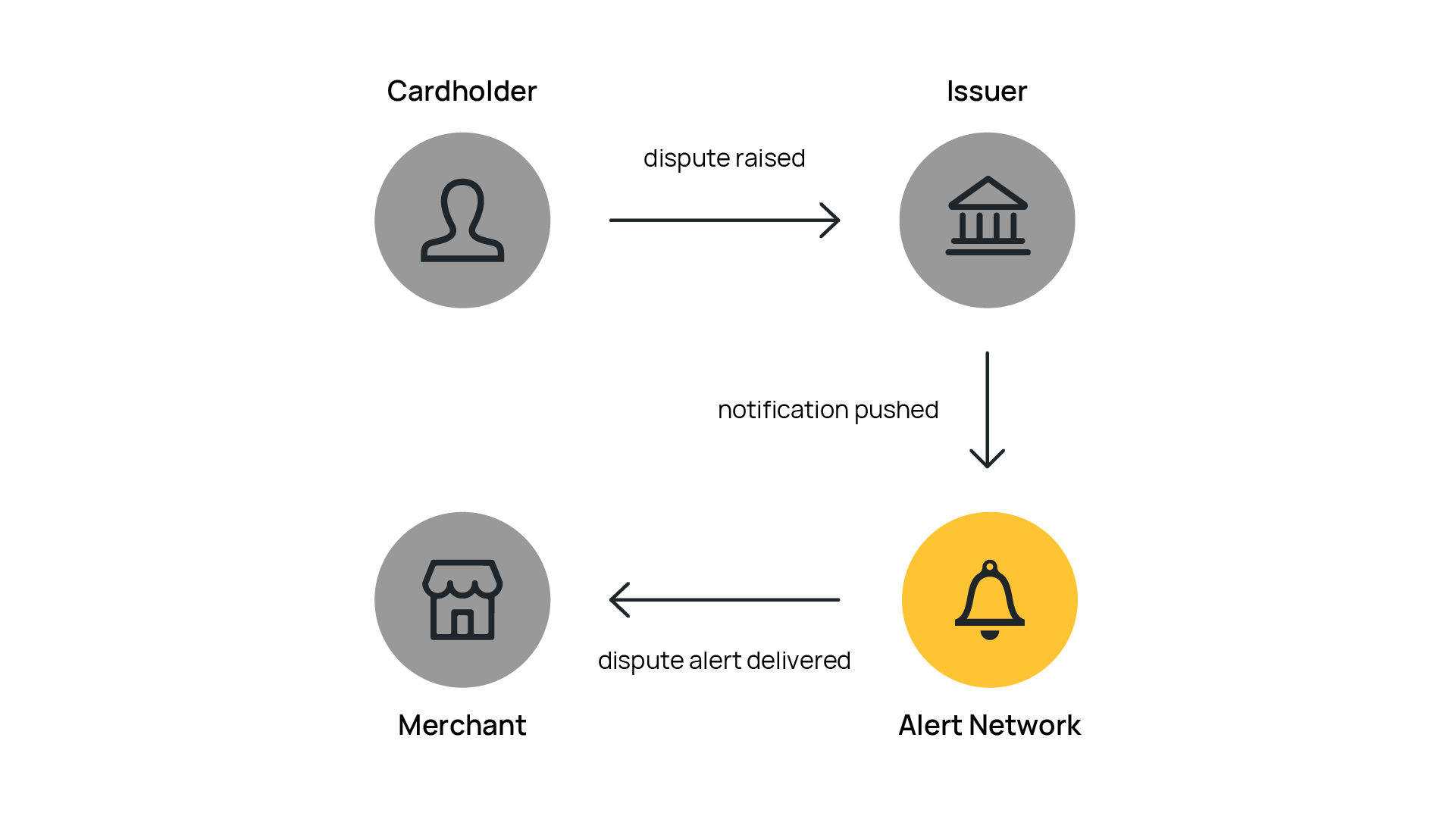

Chargeback alert programs give merchants advance notice of a dispute before it becomes a formal chargeback. When a cardholder contacts their bank, the issuer sends a notification to the relevant alert network — either Ethoca (Mastercard) or Verifi (Visa) — which delivers it to the merchant within hours. Responding within the alert window, typically 24 to 72 hours, with a refund or cancellation resolves the dispute entirely, with no chargeback fee and no impact on your chargeback ratio.

The main programs are Ethoca Alerts, which cover all major card networks through a single integration; Verifi's Rapid Dispute Resolution (RDR), which automatically resolves qualifying Visa disputes using pre-configured rules in under a second; and Verifi's Cardholder Dispute Resolution Network (CDRN), which gives merchants up to 72 hours to review and respond to Visa-side disputes. Most merchants seeking comprehensive coverage enroll in all three, with Ethoca handling cross-network volume and Verifi's tools covering the Visa-specific layer in different ways.

Chargeback Alerts and Prevention Tools: A Complete Merchant Guide

Any merchant will know that chargebacks have always been a reactive problem. By the time one lands on your desk, the merchandise has shipped, the customer has moved on, and your options for resolving the situation without cost are limited to building a representment case and hoping the evidence holds up, or writing it off as a loss. For most merchants, this is the only version of dispute management they know — waiting, responding, and absorbing losses along the way.

Alert networks fundamentally change that dynamic. Instead of waiting weeks for a formal chargeback notification to arrive, merchants enrolled in these programs receive a pre-dispute alert within hours of a cardholder contacting their bank, giving them a window to act before a chargeback is ever filed. In many cases, issuing a refund in response to that alert is all it takes to resolve the dispute entirely, with no chargeback fee, no ratio impact, and no need for representment.

What's the Difference Between a Dispute and a Chargeback?

A dispute is when a cardholder contacts their issuing bank to challenge a transaction. A chargeback follows the dispute, and is the stage where the issuing bank reviews the claim and initiates a formal reversal of the transaction. Merchants can prevent disputes from turning into chargebacks by implementing alert and prevention safeguards.

The ecosystem of tools available to merchants today spans two major alert networks — Ethoca (Mastercard) and Verifi (Visa) — alongside data-sharing programs that work further upstream to prevent disputes from being initiated in the first place. Each tool serves a distinct function, covers different transaction types, and requires different operational decisions from the merchant. Understanding how they work individually, how they interact, and how to implement them effectively is essential for any business dealing with meaningful dispute volumes.

This page covers all of it: How alert networks operate, the detailed mechanics of each major program, how to compare and choose between them, how to integrate and respond effectively, and how to calculate whether the investment makes sense for your business, giving you the complete picture before you decide where to focus.

How Do Chargeback Alerts Work?

The chargeback lifecycle is slow by design. A cardholder contacts their bank, the issuer reviews the dispute, raises a chargeback, and the notification eventually reaches the merchant, often long after the original transaction. By that point, recovering the loss requires contesting the dispute via the expensive and time-consuming representment process.

Chargeback alerts interrupt this cycle at its earliest point. When a cardholder contacts their bank about a transaction they want to dispute, the issuer pushes a notification to the relevant alert network. That network then identifies the merchant associated with the transaction, using billing descriptor matching and card data, and delivers an alert through the merchant's portal, API, or integrated platform. The merchant then has a specific window — typically between 24 and 72 hours depending on the program — to review the case and decide how to respond.

If the merchant issues a refund within that window, the issuer withdraws the dispute, and no chargeback is ever filed. No fee is charged, the transaction doesn't count against the merchant's chargeback ratio, and the customer gets their money back without the dispute escalating further. If the merchant takes no action, the window closes and the issuer proceeds with a standard chargeback as if the alert had never been sent.

Ultimately, this alerting mechanism gives merchants a second chance to resolve a dispute that would otherwise become a chargeback and benefits all involved parties:

- From the issuer's perspective, it reduces the administrative overhead of processing formal disputes.

- From the cardholder's perspective, refunds tend to come faster.

- From the merchant's perspective, it replaces a costly, uncertain process with a routine refund that preserves processing health.

There’s an important nuance here: Refunding in response to an alert is not the same as admitting liability or accepting a chargeback.

The refund is initiated by the merchant proactively, before any formal chargeback is lodged. In the networks' accounting, it is treated as a merchant-initiated credit, not a chargeback reversal, and it carries none of the ratio consequences that a chargeback would.

This is what makes alerts extremely valuable: They convert a high-cost dispute outcome into a lower-cost refund outcome, and they do so at a point when the merchant still has choices.

Ethoca Alerts (Mastercard)

Ethoca, now owned by Mastercard, is the largest and most widely used chargeback alert network in the world. Founded in 2005 and acquired by Mastercard in 2019, Ethoca built its network to connect issuers and merchants in real time so that confirmed fraud and dispute data can be shared before a chargeback is filed.

Today, the Ethoca network encompasses most major U.S. issuers and a substantial portion of global banks, making it the default starting point for any merchant building out an alert program.

What Are Ethoca Alerts and How Do They Work?

When a cardholder contacts their bank to report a transaction as fraudulent or disputed, the issuer verifies the claim and then pushes cardholder-confirmed fraud or dispute data to Ethoca.

Ethoca then matches this data to the relevant merchant using billing descriptor information and card details, and delivers the alert to the merchant's integrated system or portal. The whole process, from the cardholder's call to the merchant's notification, typically takes minutes to hours rather than the days or weeks of the traditional chargeback process.

Once an alert is received, merchants typically have a 24 to 48 hour window to respond. The response options and their consequences are covered in detail below, but the core principle is that any resolution initiated within this window — a refund, a cancellation, an account closure — prevents the chargeback from being filed.

What Card Networks Does Ethoca Cover?

One of the most significant features of Ethoca Alerts is the breadth of card network coverage it provides through a single integration.

Unlike some alert tools that are specific to a single network, Ethoca handles disputes across Visa, Mastercard, American Express, and Discover transactions through one system. Merchants don't need to enroll separately with each card scheme or manage multiple alert feeds — a single Ethoca connection covers the full range of card types that most businesses accept.

This is great news for merchants with mixed transaction volumes across card types, or those operating in markets where Visa and Mastercard share relatively even market shares. Rather than building out separate integrations and monitoring separate dashboards, Ethoca consolidates everything into one stream.

Issuer participation is extensive, too. Most large U.S. issuers are active on the Ethoca network, which translates into meaningful alert coverage from day one of enrollment. The network has continued to grow internationally as well, with European and Asia-Pacific issuer participation increasing significantly since the Mastercard acquisition.

I’ve Received An Ethoca Alert, What Do I Do?

The most common response to an Ethoca Alert is a straightforward full refund. The merchant returns the transaction amount to the cardholder, reports the resolution to Ethoca, and the issuer withdraws the pending dispute.

In most cases, this is the right call because it resolves the situation cleanly, protects the ratio, and costs only the transaction value rather than the transaction value plus chargeback fees, monitoring program penalties, and representment overhead.

Beyond refunding, the appropriate response depends on your business type and the nature of the disputed transaction. The main options are:

- Stop or cancel fulfilment. If an order hasn't shipped yet, cancelling it avoids both the chargeback and the cost of the merchandise. Even if it has shipped, initiating a return or recall may be worthwhile depending on the order value.

- Close or suspend the account. For subscription and digital goods merchants, an alert tied to a compromised account is an opportunity to cut off fraudulent access immediately, before further charges accumulate over days or weeks.

- Run link analysis. Ethoca's link analysis capability allows merchants to identify related fraudulent orders placed from the same card, device, or account, making it possible to proactively cancel or refund a cluster of fraudulent orders before any of them reach chargeback stage.

Ethoca estimates that merchants using the network stop fraud in up to 40% of alert cases. The program has contributed to avoiding more than 110 million chargebacks since its 2005 launch, and Mastercard's published data puts the total fraud value stopped through Ethoca at approximately $977 million through 2023 alone.

Ethoca Alerts and Your Chargeback Ratio

The ratio protection that Ethoca Alerts provide is one of their most valuable operational benefits.

Card networks calculate chargeback ratios — the metric used to determine whether a merchant is operating within acceptable thresholds under programs like Visa's VAMP or Mastercard's ECM — based on the number of formal chargebacks received relative to total transactions. Refunds issued in response to Ethoca Alerts are not counted as chargebacks in these calculations.

This means that a merchant with a dispute rate that is approaching a monitoring threshold can use alert programs to intercept disputes before they become ratio-damaging chargebacks, buying time to address the underlying causes without triggering program penalties. It doesn't solve a fraud or friendly fraud problem at its root, but it provides meaningful protection while longer-term fixes are implemented.

What is a Chargeback Ratio?

A chargeback ratio is the percentage of your transactions that end in a chargeback. If, for example, you processed 10,000 transactions in a month and received 50 chargebacks, your ratio would be 0.5%. That sounds small, but it's a significant amount in the eyes of card networks like Visa and Mastercard.

How Can Merchants Implement Ethoca Alerts?

Ethoca is accessible through a web portal for lower-volume merchants, or via a direct API integration for those who want to automate their alert handling at scale.

Via API, the workflow can be fully automated: an incoming alert triggers a lookup against the merchant's order management system, the relevant order is identified, a predefined response is executed — refund, cancellation, account action — and the outcome is reported back to Ethoca without any manual intervention. For high-volume merchants, this level of automation is essential because manual alert handling at any meaningful scale becomes operationally unsustainable quickly.

Many merchants choose to manage their Ethoca integration through a third-party platform rather than building a direct connection. ChargebackStop, as an authorised Ethoca reseller, integrates directly with the Ethoca network and centralises alert management alongside Verifi and other tools in a single dashboard. This removes the need to maintain multiple direct integrations, ensures that alerts from different networks are handled consistently, and provides consolidated reporting across the full alert and dispute lifecycle.

Verifi (Visa) — RDR and CDRN

Verifi is Visa's dispute prevention platform, acquired by Visa in 2019 and now the primary mechanism through which Visa-side pre-dispute alerts and automated resolutions are delivered to merchants.

Where Ethoca operates as a single alert type across multiple card networks, Verifi offers two distinct tools — Rapid Dispute Resolution (RDR) and the Cardholder Dispute Resolution Network (CDRN) — that operate differently, cover different scenarios, and suit different merchant profiles. Understanding the distinction between them is important for building an effective Visa-side dispute prevention strategy.

Rapid Dispute Resolution (RDR)

Merchants who enroll in RDR configure a set of resolution rules inside Verifi's system, defining the conditions under which they're willing to automatically credit a transaction. These rules can be built around factors including transaction amount, product category, and dispute reason code.

When a qualifying Visa dispute comes in that matches those rules, the network resolves it with a credit, in many cases in under one second. No notification reaches the merchant's operations team, no review is required, and no chargeback is ever filed: It just works automatically in the background.

Because RDR runs over existing Visa messaging infrastructure, it requires no changes on the issuer side. Issuers that participate in Visa's dispute network automatically route qualifying cases through RDR when the receiving merchant is enrolled.

RDR works best for merchants dealing with high volumes of predictable friendly fraud, which is the kind of dispute where a fast refund is the right outcome regardless. The business types that tend to benefit most are:

- Subscription businesses, where recurring billing confusion drives a large share of disputes.

- Digital goods merchants, where there's no physical product to recover and a quick credit is almost always the practical resolution.

- Direct-to-consumer brands with high order volumes and consistent dispute patterns that lend themselves to rule-based automation.

The main limitation is that RDR requires clear, defensible resolution rules. Configure them too broadly and you risk refunding transactions you could have won through representment. Configure them too narrowly and RDR captures only a fraction of your Visa disputes.

Getting the configuration right takes upfront analysis of your historical dispute data, so it's worth investing that time before deployment rather than running generic rules and adjusting reactively.

Cardholder Dispute Resolution Network (CDRN)

CDRN operates on a more protracted timeline and a broader scope than RDR. Rather than an automated resolution triggered by pre-configured rules, CDRN delivers an issuer-initiated alert that gives the merchant time to review and respond before the dispute proceeds.

When an issuer receives a dispute, instead of immediately processing it as a chargeback, they route it to the enrolled merchant as a CDRN notification. The merchant has up to 72 hours to review the case and issue a refund if they choose to. If a refund is issued within the window, the dispute is resolved without a chargeback being filed and without fees applying. If no action is taken, the issuer proceeds with a standard chargeback once the window expires.

Unlike RDR, CDRN covers both Visa transactions and some non-Visa transactions, depending on issuer participation and network configuration. It also preserves the merchant's ability to review individual cases before committing to a refund, which is particularly important for merchants whose dispute mix includes a meaningful proportion of cases where the chargeback could be won through representment.

CDRN is especially valuable for merchants who want the protection of pre-chargeback alerts without giving up oversight of the resolution process. Where RDR is inherently set-and-forget, CDRN keeps the merchant in the loop on each case. With CDRN, however, the tradeoff is that someone on the team needs to be monitoring and responding to CDRN alerts consistently, because ignoring them within the window is functionally the same as ignoring them entirely.

RDR vs. CDRN — Which is Best?

Honestly, it’s not a binary choice, and neither one is “better” than the other.

Many merchants run both simultaneously, using RDR to handle high-confidence, clearly defined cases automatically and CDRN to catch the remainder where a review window is preferred, such as high-value disputes. In this configuration, RDR acts as a first filter, resolving disputes that match the merchant's pre-set criteria in under a second, and CDRN provides a safety net for disputes that fall outside those parameters.

For merchants deciding where to start, the question to ask is whether you have the historical dispute data and operational clarity to configure RDR rules confidently. If you do, starting with RDR for your most predictable dispute types and adding CDRN coverage for everything else is a sensible approach.

If, however, your dispute patterns are variable or you're new to alert programs, starting with CDRN gives you visibility into the nature of your pre-dispute cases before you commit to automated resolution logic.

The 2025 RDR Pricing Update

Verifi's standardised $19 per alert pricing for RDR, introduced in 2025, is an important factor in any ROI calculation for merchants evaluating the program.

At $19 per resolved alert, whether RDR is worthwhile for you depends significantly on the average value of a prevented chargeback, including the dispute fee, the transaction value at risk, and any monitoring program costs that a chargeback would contribute to.

For merchants where the all-in cost of a chargeback regularly exceeds $75 to $100, RDR at $19 per resolution is highly cost-effective. For merchants with very low average transaction values, it's worth modelling the numbers against your actual dispute data before committing.

How Can Merchants Enrol in Verifi?

Merchants activate Verifi tools through their acquirer or directly via the Verifi API and Visa Resolve Online portal. Order data and dispute decision routing need to be configured as part of the integration. For RDR in particular, the resolution rules need to be built before the system can operate. Luckily, many payment gateways have built-in Verifi connectivity, which simplifies the technical side of enrollment considerably.

Alternatively, you can work with a third-party reseller. ChargebackStop's direct authorisation as a Verifi reseller means that merchants connecting through the platform benefit from official network access, compliant alert delivery, and centralised management alongside Ethoca and other tools — all without needing to build or maintain separate Verifi and Ethoca integrations independently.

Preventing Chargebacks Upstream

Alert networks like Ethoca and Verifi intercept disputes after a cardholder has already decided to contact their bank. However, the data-sharing tools that sit alongside them (Visa's Order Insight and Mastercard's Ethoca Consumer Clarity) work further upstream, aiming to prevent the cardholder from initiating a dispute in the first place.

Visa Order Insight

Order Insight works by transmitting detailed transaction data from the merchant to Visa at the time of each transaction. If a cardholder later contacts their bank about an unrecognised charge, the issuer's app or call centre can retrieve an itemised receipt, the merchant's logo, the purchase date, the items bought, and other contextual details sourced directly from the merchant's transaction data. When a customer can see exactly what they purchased and when, a large proportion of "I don't recognise this charge" disputes simply don't proceed.

Visa reports that global merchants using Order Insight deflect between 40% and 45% of confirmed first-party misuse disputes, which are disputes where the cardholder is a genuine customer who simply failed to recognise the charge. For subscription businesses, where recurring billing confusion is a leading cause of disputes, deflection rates as high as 90% have been observed.

These numbers reflect the reality that a meaningful share of all chargebacks are filed not because the customer is dissatisfied or acting fraudulently, but because they can't identify the charge on their statement. This is known as first-party or “frienly” fraud, and giving them that information before a dispute is filed eliminates the problem at its source.

What is Friendly Fraud?

Friendly fraud (also called first-party or chargeback fraud) is where a cardholder disputes a legitimate charge to get a refund. Unlike traditional fraud, where a criminal uses a stolen card, friendly fraud is committed by the actual cardholder. It's called "friendly" fraud because the customer is known.

Order Insight is free for merchants, because Visa has an interest in reducing the volume of disputes flowing through its network. Merchants who wish to use it, however, must transmit detailed order metadata alongside each transaction via their payment gateway or acquirer. Once the data pipeline is set up, the program operates passively, with no alert management or active merchant response required.

Ethoca Consumer Clarity

Ethoca Consumer Clarity is Mastercard's equivalent, sharing rich purchase information through issuers' apps and call centre systems. Where Order Insight operates on the Visa side, Consumer Clarity covers Mastercard transactions using the same underlying principle: Give customers clear, recognisable transaction records so they don't need to dispute charges they simply can't identify.

Consumer Clarity operates similarly to Order Insight, with merchants being required to supply transaction metadata via API or integration, and the data becomes available to issuers when cardholders enquire. The merchant doesn't need to take any action on a per-dispute basis. Mastercard data indicates that programs like Consumer Clarity can contribute to a 20% to 25% reduction in chargeback volume among participating merchants, primarily through the elimination of confusion-driven disputes.

Used together, Order Insight and Consumer Clarity address what is consistently one of the highest-volume causes of chargebacks — unrecognised transactions — without any ongoing operational overhead from the merchant side once the data integration is in place.

Comparing the Major Alert Solutions

With multiple programs available, each with different mechanics, coverage, and cost structures, it's worth laying out how they all differ.

- Ethoca Alerts cover all major card networks through a single integration, deliver near-real-time notifications based on issuer-confirmed dispute data, and give merchants a 24 to 48 hour window to respond. They are the broadest-coverage option available and the most practical starting point for merchants who want alert protection across their full transaction volume regardless of card type.

- Verifi RDR is Visa-specific, operates in real time through automated rule-based resolution, and requires no merchant action once rules are configured. Its sub-second resolution capability makes it uniquely effective for high-volume friendly fraud scenarios, but the $19 per alert pricing introduced in 2025 means it works best where the average cost of a prevented chargeback is substantially higher than the alert fee.

- Verifi CDRN is broader than RDR in scope, covering Visa and some non-Visa transactions, and gives merchants up to 72 hours to review and respond. It preserves merchant oversight on a per-case basis, making it suitable for merchants who want visibility into individual disputes rather than automated blanket resolution.

Building Full Coverage Across Networks

Merchants seeking comprehensive alert coverage typically enroll in both Ethoca and Verifi's programs.

Ethoca handles the cross-network layer, covering Visa, Mastercard, Amex, and Discover disputes from participating issuers. Verifi's RDR and CDRN add Visa-specific coverage that captures cases not covered by the issuers enrolled in Ethoca, and the automated resolution capability of RDR handles a category of dispute volume that Ethoca's alert model doesn't address.

The combination means that a qualifying Visa dispute might be resolved by RDR in under a second, a qualifying Mastercard dispute might generate an Ethoca Alert for merchant review, and a broader Visa dispute not covered by RDR might arrive as a CDRN notification. Together, the programs cover significantly more of the pre-chargeback dispute process than any single tool can reach alone.

Can Merchants Can Set Up Their Own Chargeback Alerts?

In short: yes. Most major acquirers and payment processors offer Ethoca and Verifi connectivity as built-in options, and for merchants with straightforward processing arrangements, enrollment can often be completed directly through existing gateway settings.

The core requirement for any API-based integration is reliable transaction matching. When an alert arrives, your system needs to identify the corresponding order by matching on transaction ID, card number fragment, amount, and date, and trigger a response before the window closes. At scale, this logic needs to be fully automated. Any manual step in the matching process risks burning through the available response window on lookup tasks rather than resolving the actual dispute.

Merchants running multiple gateways face an added layer of complexity, because each gateway connection needs to feed into the same alert management workflow. Building and maintaining separate integrations for Ethoca and Verifi, across multiple processors, adds meaningful overhead and introduces coordination risks between alert streams.

As you can imagine, this can become quite a technical process, especially if you're managing a lot of gateways and have high transaction volumes. Sure, lower-volume merchants can manage alerts through a web portal without any API work, but at higher volumes, manual handling becomes unsustainable quickly, and automation is the only practical alternative.

That's why we always recommend that merchants work with authorized resellers who can manage chargeback alert implementation and ongoing maintenance, leaving them to focus on responding to disputes quickly as they come in

ChargebackStop is an authorized reseller of both Ethoca and Verifi, which means merchants connecting through the platform get direct, compliant access to both networks through a single integration. This eliminates the need for separate gateway-level configurations, indirect routing, and managing two alert streams in parallel. Transaction matching is handled automatically across integrations with Stripe, Adyen, Shopify, Authorize.Net, Revolut, NMI, ACI, and Fiserv, so alerts arrive alongside the relevant order context without any manual reconciliation work from your team.

Invalid alerts are automatically flagged and credited, so you're only paying for cases that represent genuine, actionable disputes. On average, between 5 and 10% of monthly alerts fall into this category, a saving that accumulates quickly for businesses processing alerts at volume.

Get smart chargeback alert coverage, fast

ChargebackStop clients report preventing 95% of enrolled disputes before they reach chargeback stage, and a 60% reduction in dispute-related operational hours after implementation.

Chargeback Prevention FAQs

Straight answers to the questions merchants actually ask about chargeback alert tools.

When a cardholder contacts their bank to dispute a transaction, the issuer pushes a notification to the relevant alert network before processing a formal chargeback. That network identifies the merchant associated with the transaction and delivers an alert through their integrated platform or portal, typically within minutes to hours of the cardholder's call. The merchant then has between 24 and 72 hours to review the case and respond. If a refund is issued within that window, the dispute is resolved without a chargeback being filed — no dispute fee, no ratio impact.

Ethoca is a cross-network alert service, meaning a single integration covers disputes across Visa, Mastercard, American Express, and Discover transactions from participating issuers. Verifi is Visa's own dispute prevention platform and operates through two distinct tools: RDR, which automatically resolves qualifying Visa disputes using rules you configure in advance, and CDRN, which delivers issuer-initiated alerts with a response window for merchant review.

The programs are complementary rather than competing — Ethoca covers cross-network volume through a merchant-response model, while Verifi's tools add Visa-specific coverage with automation options that Ethoca's model doesn't offer.

Running both programs together provides significantly broader coverage than either achieves alone. Ethoca handles disputes from participating issuers across all major card types, while Verifi's RDR and CDRN capture Visa-side cases that fall outside what Ethoca covers due to issuer participation gaps.

In practice, a qualifying Visa dispute might be resolved automatically by RDR, a Mastercard dispute might trigger an Ethoca Alert for merchant review, and a broader Visa case might arrive as a CDRN notification. Merchants with meaningful dispute volumes across card types generally find that the combination covers substantially more of their pre-chargeback exposure than any single program can reach.

Refunds issued in response to chargeback alerts are not counted as chargebacks by the card networks. Because the refund is processed before any formal chargeback is filed, it's treated as a merchant-initiated credit rather than a dispute loss, and it carries no impact on your chargeback-to-transaction ratio. This matters most for merchants approaching monitoring thresholds under programs like Visa's VAMP or Mastercard's Excessive Chargeback Merchant program, where intercepting disputes at the alert stage prevents them from being recorded against your ratio in the first place.

Pricing varies by program and by how you access the network.

Verifi's RDR was standardized at $19 per resolved alert in 2025. For merchants where the all-in cost of a chargeback regularly exceeds $75 to $100 — including the dispute fee, transaction value, and operational overhead — RDR is typically cost-effective at that rate.

Ethoca Alert pricing varies depending on your volume and access method, whether that's a direct integration, your acquirer, or an authorized reseller. One factor worth understanding is that not every alert represents a genuine, actionable dispute. Between 5-10% each month tend to be duplicates or invalids, so working with an authorized reseller that automatically identifies and credits invalid alerts means you're only paying for disputes that actually warrant a response.