Visa’s VAMP Program: What Merchants Need to Know About the New Dispute & Fraud Rules

Visa’s updated Acquirer Monitoring Program (VAMP), which launched in April 2025, fundamentally changes how Visa tracks and enforces dispute (chargeback) and fraud rates. It replaces the old Visa Fraud Monitoring Program (VFMP) and Visa Dispute Monitoring Program (VDMP), consolidating them into one unified framework.

How Does VAMP Work?

Under VAMP, Visa now measures both fraud (TC40 reports) and all disputes (TC15 chargebacks, including service disputes) together, using a single count-based ratio. This means merchants and their banks must manage one combined dispute/fraud metric instead of separate ones.

In practice, VAMP works by having Visa review each month how many transactions in your portfolio were flagged as fraud or went to dispute relative to total sales. Visa also introduced an enumeration ratio to catch card‐testing attacks: if more than 20% of your authorizations are identified as “enumerated” and exceed 300,000 in a month, you will be flagged for VAMP.

The goal is to hold both acquirers and merchants to tighter risk standards. Now, Visa monitors portfolios at the acquirer level, making banks responsible for the aggregate risk across all their merchants. If an acquirer breaches these thresholds, Visa can enforce remedies across the whole portfolio, rather than penalizing one merchant in isolation.

For merchants, this means their dispute/fraud rates count toward the acquirer’s performance. High‐chargeback merchants can push an acquirer into the VAMP program, so acquirers will likely pressure risky merchants to clean up their fraud controls.

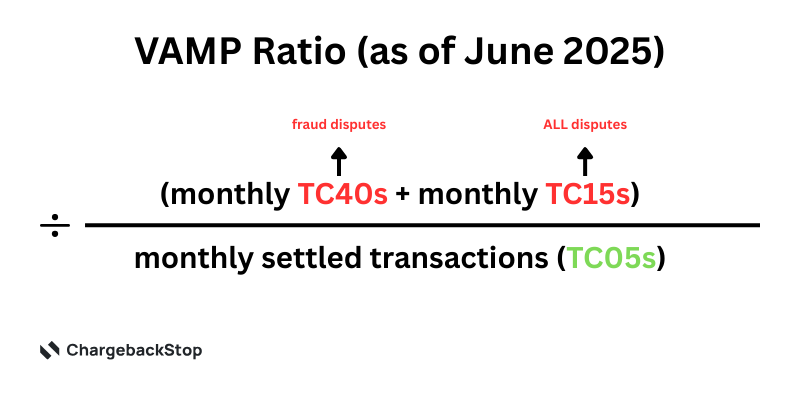

How VAMP Metrics are Calculated

Under the new VAMP rules, Visa counts all chargebacks and fraud reports, whether the reason was fraud or not, in the ratio. Previously, some dispute reason codes (e.g., 10.XX on Visa, often fraud-related) were excluded. Now they are included.

The official formula per Visa is:

Importantly, Visa explicitly excludes disputes resolved through pre-dispute alert tools (like Verifi RDR) and fraud cases won with Compelling Evidence 3.0 if those are fully resolved within the same calendar month as the initial report was filed. In other words, using alert networks and resolution services is now more rewarding; resolved transactions do not count against your VAMP ratio.

The enumeration ratio is calculated separately as:

- Enumeration Ratio = (Count of enumerated auths) ÷ (Count of total auths)

If that exceeds 20% and at least 300,000 auths in a month, Visa flags the account for card‐testing attacks. Merchants that suffer heavy “card testing” must use fraud tools to identify and block those attacks, or risk VAMP enrollment.

New Threshold Tiers: Above Standard and Excessive

VAMP establishes “Above Standard” and “Excessive” levels, mostly for acquirers; merchants have only an Excessive tier in the new system. These are based on the ratio described above, with additional volume and geography criteria. For example:

- Acquirers (Portfolio Level) — Visa labels an acquirer’s portfolio as Above Standard at a VAMP ratio of ≥0.5% and <0.7% and Excessive at ≥0.7%. Both thresholds require the portfolio to exceed a minimum count of TC40 plus TC15 events (1,500 incidents per month in most regions). Visa will begin enforcement of these thresholds from January 1, 2026.

- Merchants — There is no separate “Above Standard” tier for merchants, only Excessive. A merchant’s account is flagged as Excessive if its VAMP ratio exceeds a set threshold and it passes minimum volume, typically 1,500 TC40 plus TC15 transactions per month, or 150 transactions totaling more than $75,000 in some regions. For most markets (Americas, Europe, APAC), the Excessive merchant threshold starts at 2.2% of sales from June 1, 205, then drops to 1.5% on April 1, 2026.

Above the Excessive threshold, Visa may review individual merchants in the portfolio. For example, if an acquirer’s portfolio goes Excessive, Visa may look at which merchants are causing the issue. The new schema is more granular than before: It replaces the old 1.8% dispute and fraud cut-offs and the $250,000 fraud limits of VDMP/VFMP with this tiered system.

Consequences of Exceeding VAMP Thresholds

Falling into the VAMP program has real costs. Visa provides an advisory period through September 2025, but starting October 1, 2025, penalties kick in for any breaches. Acquirers labeled Above Standard incur fines of $5 per disputed/fraudulent transaction in excess, and Excessive acquirers get $10 each. Similarly, any merchant deemed Excessive is fined $10 per qualifying transaction. These fines are on top of the usual chargeback fees and represent a serious drag on margins.

In other words, every additional dispute or fraud after the threshold is effectively a surcharge. In some markets, Visa may reduce or waive fines if the acquirer already charges an unsecured dispute fee, but that isn’t universal.

The stakes for merchants extend beyond fees. Historically, merchants that chronically exceed chargeback programs risk losing their acquiring relationship entirely. Under VAMP, banks and processors have even more incentive to push out high-risk clients. Visa’s policy notes explicitly warn that persistent violations can lead banks to “freeze or terminate” merchant accounts.

Implications for Merchants and Acquirers

The new VAMP rules mean merchants must be more proactive than ever. Instead of reacting to chargebacks, businesses need to prevent and preempt them. Acquirers will hold their merchants accountable: A merchant’s fraud/dispute rate now directly affects the acquirer’s standing. Key actions for merchants include:

- Monitor your VAMP ratio closely. Compare your TC40 plus TC15 rate to the new VAMP formula and thresholds. Determine if spikes in fraud or friendly fraud (like “item not as described” claims) could push you into excess territory.

- Use pre-dispute alerts and resolution tools. Platforms like Verifi’s RDR or Ethoca Alerts let you resolve issues before they become chargebacks. Visa now excludes these resolved disputes from the VAMP ratio, effectively rewarding prevention. Integrating these alerts can dramatically slash your dispute counts.

- Strengthen fraud prevention. Implement robust fraud filters and evaluate your checkout processes: Merchants with higher false-decline rates might stay under VAMP, but too many declines hurt sales. Visa’s changes could incentivize merchants to swing too far in one direction. We recommend balancing fraud controls to protect revenue and keep disputes low.

- Work with your acquirer. Communicate with your bank or payment provider about how you can help them. Many acquirers will now renegotiate risk thresholds or require extra controls on accounts. Understanding your acquirer’s internal limits and dispute policies is crucial.

- Analyze dispute drivers. Recognize that Visa explicitly folded first-party (friendly) fraud disputes into the program. For instance, “item not received” or “product not as described” claims count as part of your VAMP rate. Industries hit by high first-party fraud should re-examine refund policies and customer service tactics to reduce unwarranted disputes.

Why VAMP Matters More Than Ever

Visa’s VAMP redesign reflects broader industry and regulatory pressures. Issuing banks and networks are clamping down on fraud in response to rising losses. For example, Mastercard reports that friendly fraud is surging, and has launched a “First-Party Trust” data-sharing program to help merchants and issuers exchange evidence. In parallel, regulations like the EU’s PSD2/3 frameworks are requiring better fraud reporting and shifting liability, meaning merchants and acquirers must tighten fraud controls.

Ultimately, Visa’s consolidation of VAMP signals a shift to risk-based enforcement. Instead of one-size-fits-all rules, Visa will scrutinize portfolios based on data-driven scores, including its Account Attack Intelligence system. This aligns with trends like real-time fraud scoring and data analytics in payments. However, it also means the old “warning” stages are gone; acquirers won’t get a gentle alert when they’re heading toward trouble. The thresholds and fines will be enforced strictly once the advisory period ends.

How ChargebackStop Can Help

To stay ahead under VAMP, many merchants are turning to automated tools that handle fraud and disputes seamlessly. ChargebackStop is one such solution. Our platform integrates directly with Visa and Ethoca networks to deliver pre-chargeback alerts from Verifi RDR and Ethical, and empowers merchants to act on them automatically.

By responding to alerts quickly (e.g. issuing a refund or clarification), merchants resolve issues without waiting for a formal chargeback. Crucially, Visa excludes these resolved alerts from VAMP calculation, so proactive use of alerts keeps your dispute ratio lower.

ChargebackStop also automates the representment process: If a chargeback comes in, its platform helps you gather compelling evidence and submit a persuasive response. This improves win rates and reduces your net dispute losses, which in turn helps keep your VAMP ratio down.

By leveraging these automated fraud and dispute management tools, merchants can turn Visa’s compliance requirements into an operational advantage with ChargebackStop. You’ll be notified instantly of issues, won’t lose money to frivolous disputes, and can focus on growing your business rather than firefighting chargebacks.

Want to see it in action? Contact us for a product demo.