_in_Visas_VAMP_Inflates_Your_Risk.webp)

How Double Counting (TC40 + TC15) in Visa’s VAMP Inflates Your Risk

Imagine this: You’re checking this month's fraud level for your company, when you notice that your Visa VAMP ratio has spiked. Upon further investigation, you realise that many of the fraudulent transactions are being counted twice, once as a TC40 (a fraud report) and again as a TC15, which registers as a dispute/chargeback; this is called double-counting.

Double counting has been integrated into Visa’s new VAMP formula, thus making merchant accounts appear a lot riskier than they truly are. Consequently, you may then be flagged by VAMP even if your fraud level is lower than it appears.

Here, we’ll break down what double-counting truly is, how it works, why it happens, and how to keep your ratio accurate.

What is Double Counting in VAMP?

Double-counting in VAMP is the co-occurrence of TC40 and TC15 reports for a singular fraudulent transaction.

TC40 reports occur when the customer disputes a transaction they claim is unauthorised; it is issued by the bank of the customer and is used for Early Fraud Warnings. TC15 reports - on the other hand - cover not only fraud-related instances, but any type of dispute; these turn into a formal chargeback record.

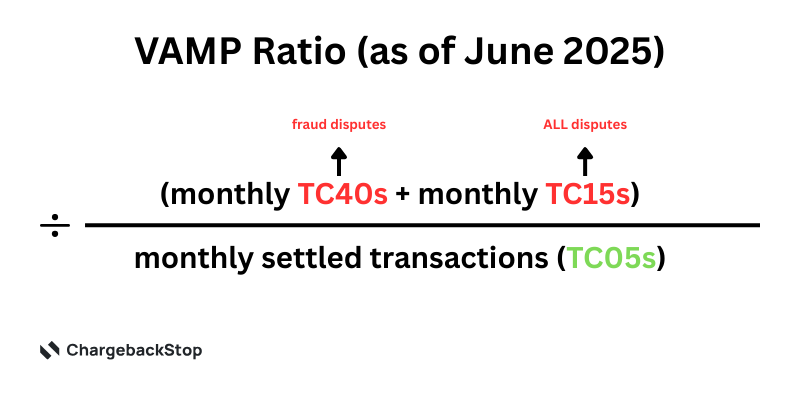

The Visa VAMP ratio formula calculates the total number of TC40 and TC15 reports for one month, divided by the total number of settled card-not-present (CNP) transactions of the same month.

Double-counting is harmful for businesses because if one occurrence of fraud is counted twice, it can rapidly inflate the numerator in Visa’s ratio. Every TC40, regardless of whether it turns into a chargeback, and every TC15 report has a direct impact on your fraud ratio.

The Formula and Its Exclusions

Visa’s official ratio formula is as follows:

Let’s break down each component of this formula:

- TC40 (fraud reports): these are instances of suspected fraud, issued by the bank on behalf of the customer.

- TC15 (disputes): these are confirmed chargebacks, covering any type of dispute, including fraud.

- TC05 (settled): these are all processed transactions.

What’s Excluded (and When)

Under ‘Compelling Evidence 3.0’, accepted evidence can suppress both the TC40 and TC15 reports. - but there’s a timing clause; exclusions depend on when the data extract is taken. If a dispute is resolved through pre-dispute processes (like RDR) before it becomes a chargeback, it will not count.

It’s important to note that these exclusions are contingent on timing, meaning some RDR cases may still slip into the ratio if processed late.

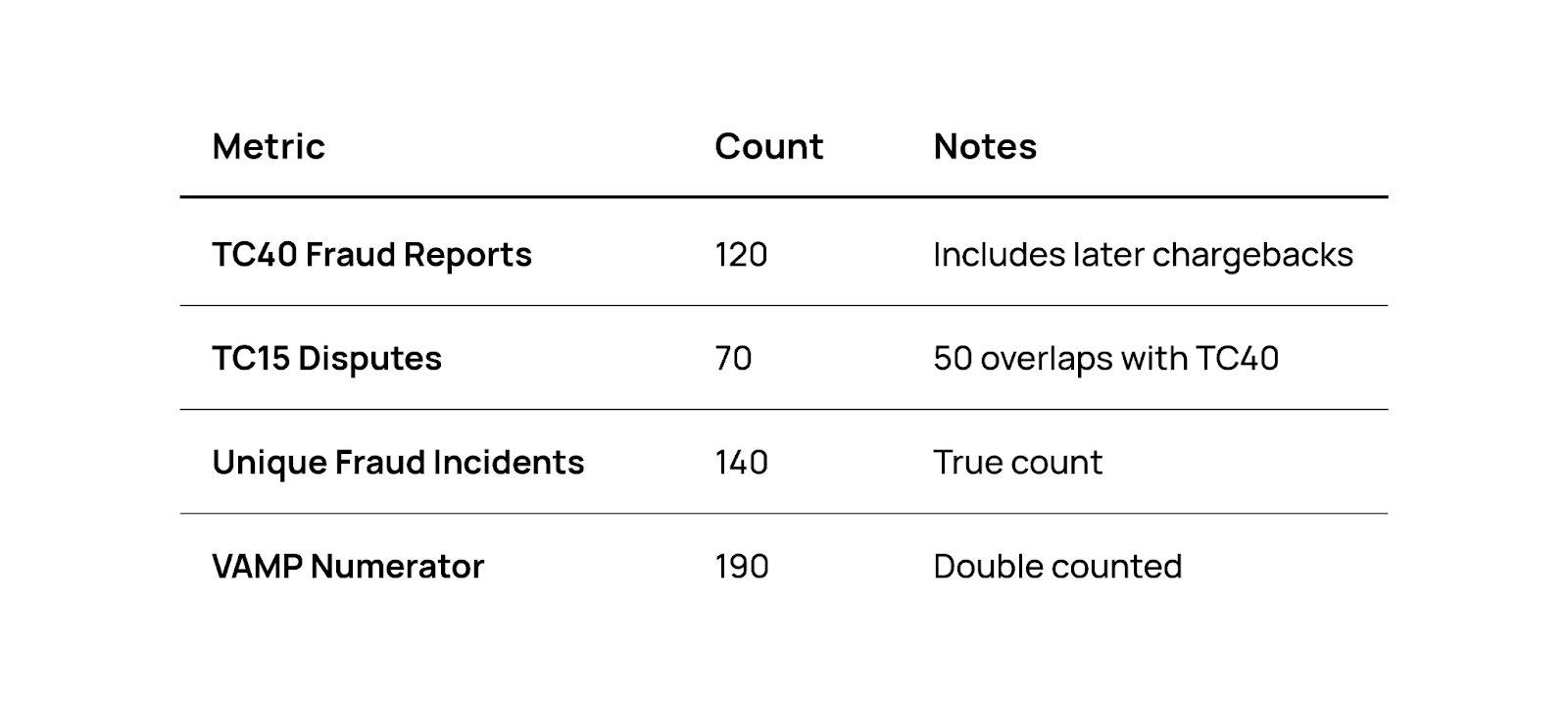

Worked Example: How Double Counting Inflates the Numbers

Imagine you have 10,000 settled transactions (TC05), 120 TC40 fraud reports and 70 chargebacks (TC15). Visa would calculate this through VAMP as: (120 + 70) ÷ 10,000 = 1.9%. But what if 50 of those 70 chargebacks actually originated from the same fraud reports (TC40)? This would mean that only 140 unique transactions were fraudulent. The extra 50 “double counts” inflated the risk by 0.5%.

Double counting can’t be ignored; it’s fraud counted twice, pulling your ratio up and credibility down.

Why Visa Counts It This Way

Visa has a clear goal to capture all fraud and dispute risk activity, regardless of if they’re unique cases.

Due to this, they treat TC40s and TC15s as distinct data streams:

- TC40 = issuer-level fraud detection.

- TC15 = acquirer dispute record.

A TC40 may turn into a TC15 (but not always) and Visa has to separate the two to ensure all instances of fraud and disputes are reported. Though this is an efficient method from Visa for network oversight, it can be damaging for merchants trying to stay below thresholds.

5 Ways to Mitigate Double Counting Risk

1. Deduplicate Fraud and Disputes Internally

Identify where the TC40 (fraud reports) and TC15 (disputes) overlap within your data and make sure these are deduplicated to prevent double-counting. Work with your acquirer to ensure this happens by cross-referencing transaction data, case IDs, and timestamps to automatically flag duplicates.

2. Resolve Issues Early with RDR

Visa’s Rapid Dispute Resolution (RDR) can automatically settle cases by offering refunds before they turn into a formal chargeback. By addressing disputes as early as possible, merchants can prevent additional fraud reports and chargebacks; this can also help avoid double-counting if the report (TC40) does not turn into a chargeback (TC15).

3. Leverage Compelling Evidence 3.0

Compelling Evidence 3.0 (CE3.0) can help prevent double-counting by preventing a formal chargeback from being filed; this is through allowing merchants to provide comprehensive transaction data to show that the cardholder previously made legitimate transactions. It can stop disputes that could have inflated your VAMP ratio.

4. Tune Fraud Controls to Prevent TC40s

TC40 reports are entirely preventable by refining fraud rules, analysing patterns of illegitimate activity to ensure that your fraud filters are apprehending real threats. The fewer TC40 reports there are, the fewer chances for duplication.

5. Monitor Timing Windows

Double-counting often occurs when TC40 and TC15 reports are filed within overlapping reporting windows. It’s important to monitor timing windows, as doing this can prevent double-counting from happening.

What to Ask Your Acquirer

Your acquirer is your first line of defense; they can help you manage how your portfolio risk is viewed - something that is vital in managing fraud.

Here are some key questions to ask your acquirer:

- How are you deduplicating TC40 + TC15 data at the acquirer level?

- When do you extract VAMP metrics for reporting?

- Are RDR and CE3.0 exclusions being properly applied?

- Can you share the overlap rate between TC40s and TC15s?

- What steps can we take together to reduce our reported numerator?

These questions can help you understand how your acquirer manages fraud and dispute data, which is critical in preventing double-counting.

TL;DR? Keep Your Ratio Accurate

It’s possible to keep your ratio accurate; VAMP’s formula counts both TC40 and TC15, meaning that a single dispute can be recorded twice, inflating your apparent risk and making your business appear worse than it truly is. However, it is possible to prevent these double hits using tools such as CE3.0 and RDR - but the timing is important. Effective deduplication and acquirer collaboration are essential to ensure your fraud levels are reflective of the true numbers. Essentially, merchants who understand and proactively manage their data will stay compliant and in control.

How ChargebackStop Helps You Fight Double Counting

Chargebackstop is here to help you avoid double-counting and appearing riskier than you truly are. Our system automatically matches TC40 and TC15 data and routes eligible cases through RDR and CE3.0 before your VAMP ratio is inflated. We also give acquirers clean, deduplicated reporting that reflects the true nature of your merchant account performance.

Want to see how much of your VAMP ratio is ‘phantom risk’? Book a demo to uncover and eliminate double-counting in your dispute data.