Most chargebacks don't begin with fraud, but rather with a customer reviewing their bank statement, seeing an unfamiliar charge, and pressing the dispute button. The transaction might be a subscription renewal they forgot about, a purchase from a sub-brand they don't recognize, or a digital product with an unhelpful billing descriptor. Without enough context to jog their memory, the path of least resistance is a dispute. Once that process begins, it becomes expensive for everyone involved.

ChargebackStop has always been built around the idea that preventing chargebacks is more effective than fighting them after the fact. Two new capabilities now extend that prevention layer earlier in the dispute lifecycle: Digital Receipts and Systematic Dispute Deflection.

They work differently, solve different problems, and are powered by different card network programs. But together, they give merchants, PSPs, and acquirers substantially more control over disputes before those disputes ever reach the chargeback stage.

Digital Receipts: Giving Issuers the Full Story

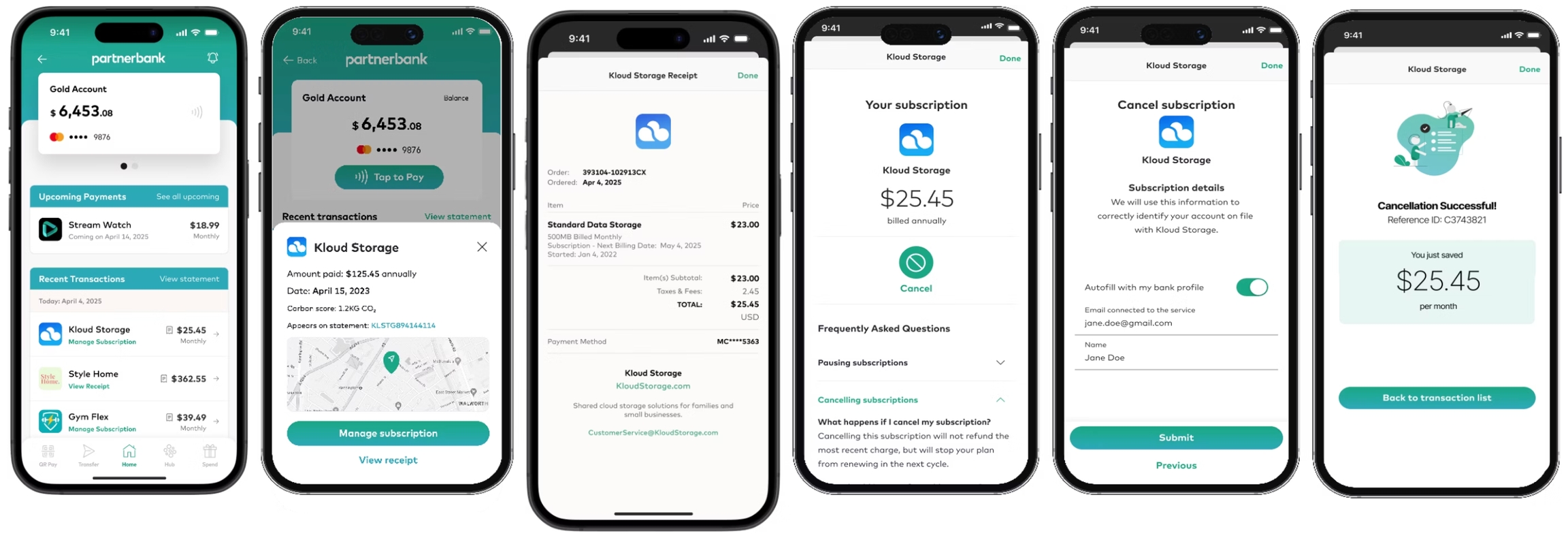

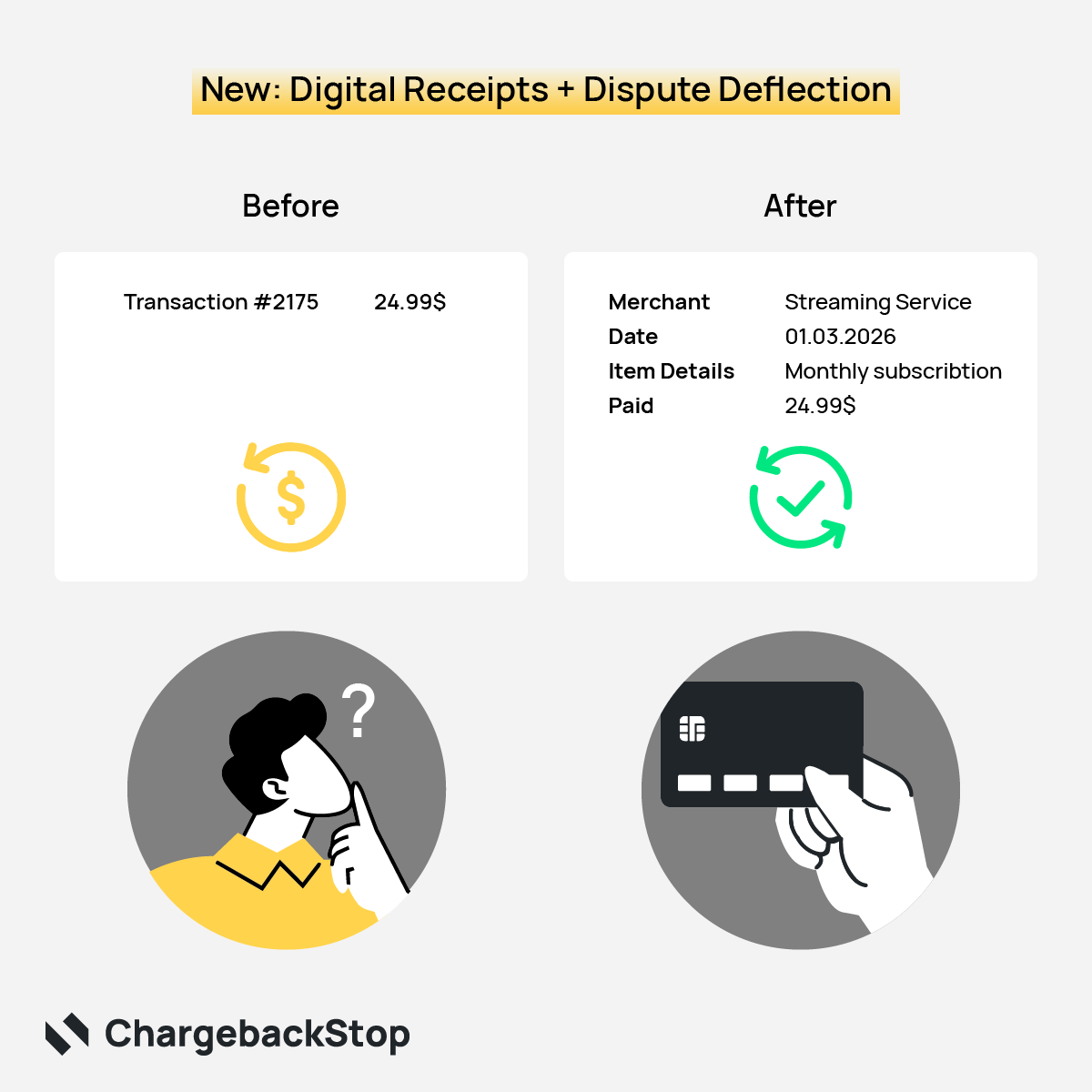

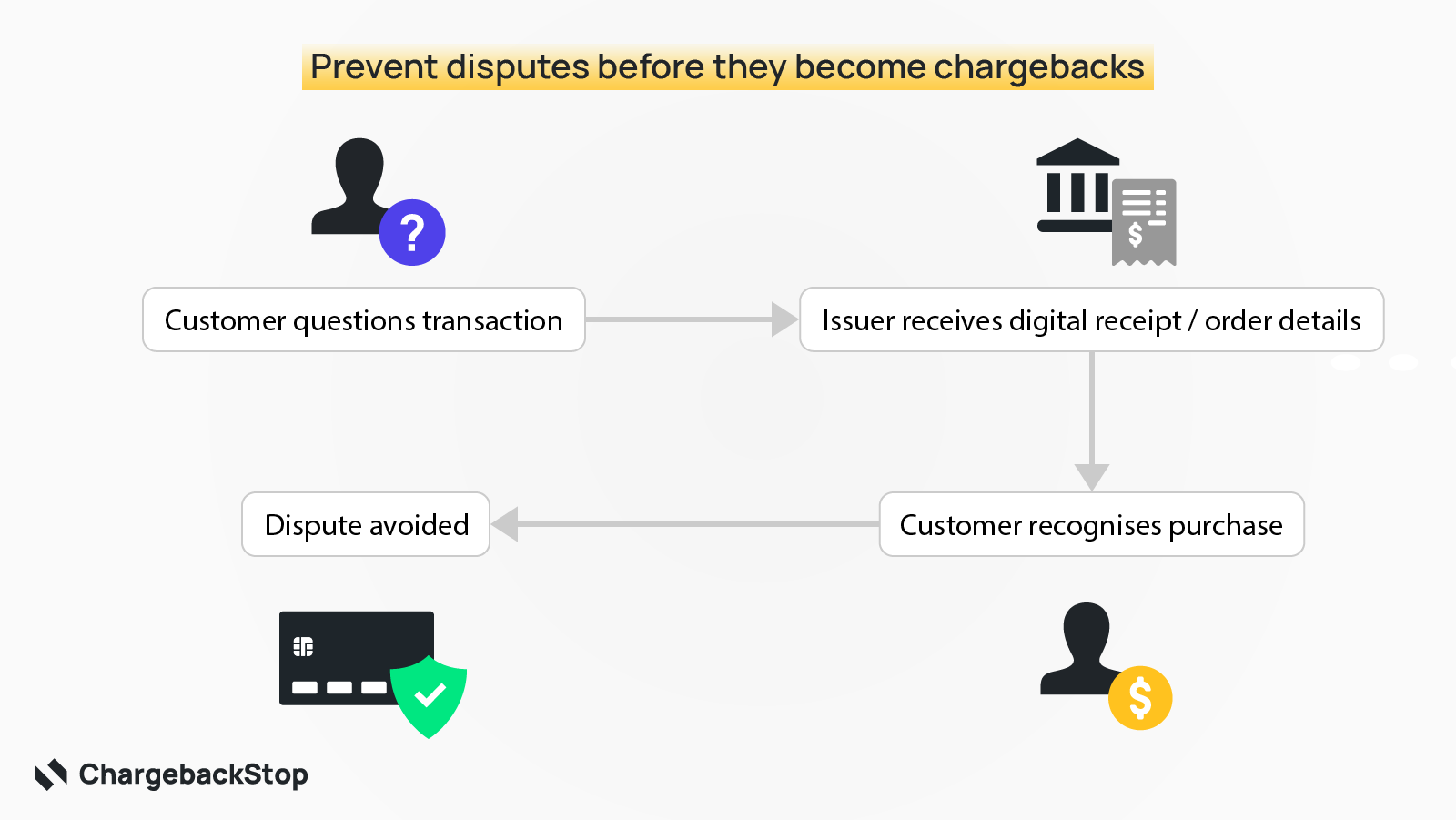

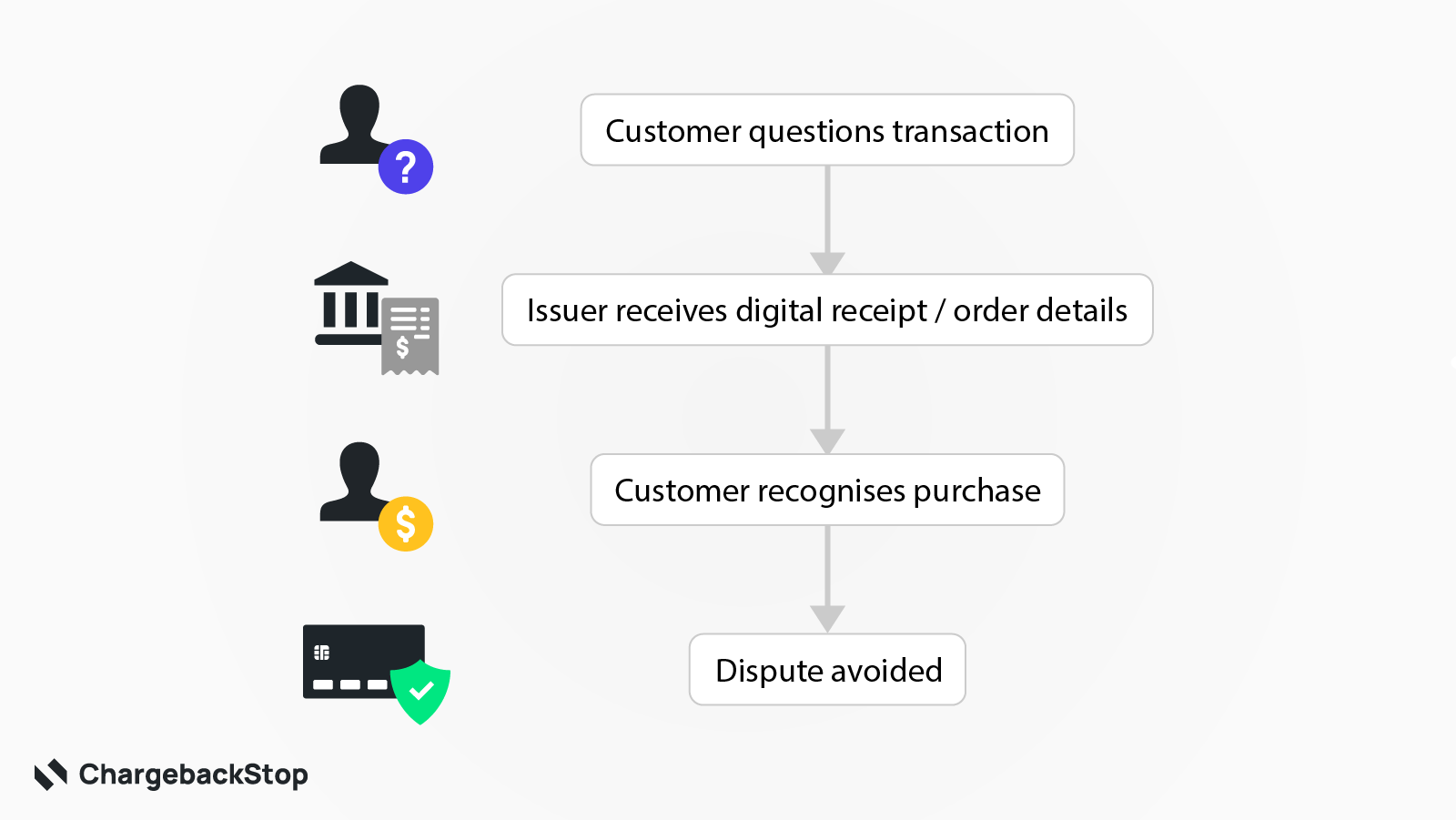

When a cardholder queries a transaction with their bank, the bank typically has very little to show them. A merchant descriptor, an amount, and a date. That's rarely enough to help someone recall a legitimate purchase, especially if weeks have passed or the descriptor doesn't obviously match the brand they bought from.

Digital Receipts change that by making detailed order information available to issuing banks in real time. When a cardholder views a transaction or a banking agent opens the dispute portal, a lookup checks whether additional data is available. If it is, the bank can display it alongside the original transaction record. This can include:

- Product or service details

- Order numbers

- Purchase dates

- Billing information

- Delivery confirmation

- Customer contact information

- Refund policies

- Supporting order data

In other words, the issuer can show the cardholder the full story behind the transaction, with each response based on what's available at the time of the query.

When customers can immediately see what they purchased, disputes often stop before they start. This is particularly valuable for industries where billing confusion is common:

- Subscription businesses dealing with renewal charges that customers forget about.

- Marketplaces and platforms with descriptors that don't clearly reflect the seller.

- SaaS and digital products that can be difficult to identify from a statement line alone.

In all of these cases, Digital Receipts can resolve the confusion before it becomes a dispute.

Systematic Dispute Deflection: Stopping Disputes Before They Escalate

Digital Receipts help with recognition by giving cardholders the information they need to remember a legitimate purchase. Systematic Dispute Deflection solves a different problem: first-party misuse, where a cardholder disputes a transaction they genuinely made.

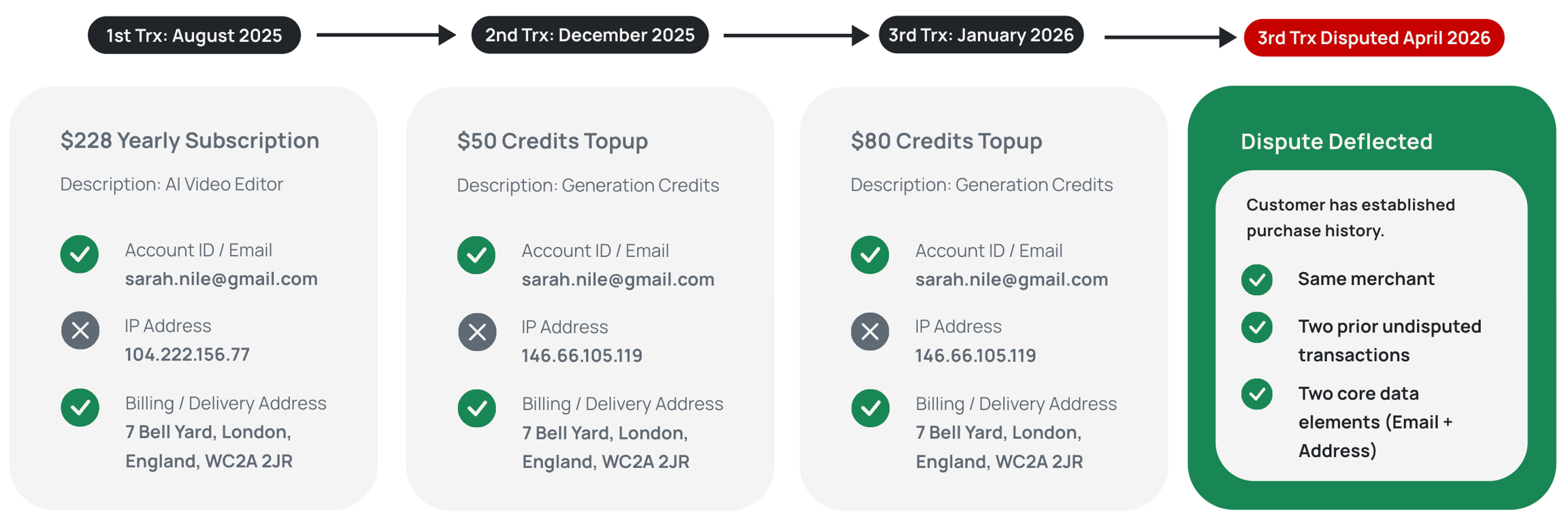

When a cardholder attempts to file a dispute, the card network performs a real-time lookup against historical transaction data that the merchant has provided through ChargebackStop.

If the cardholder has completed at least two previous transactions within 120 to 365 days of the disputed charge, and qualifying identifiers match across those transactions, the dispute is blocked at the network level before it's ever raised. The cardholder's bank never files a chargeback, no funds are reversed, and no fees are incurred.

How Qualifying Data Works

The system matches identifiers unique to the cardholder — IP address, email address, device fingerprint, and billing address — across the disputed transaction and the earlier purchase history.

At least two identifiers must match, and one of them must be either an IP address or an email address. When those criteria are met, the network treats the dispute as unjustified and blocks it outright.

Currently, deflection applies to Visa reason code 10.4 and Mastercard reason code 4814, both covering card-not-present transactions. Other conditions may become eligible as the networks expand their programs.

Implications for VAMP

The distinction between Systematic Dispute Deflection and other prevention tools becomes especially important under Visa's Acquirer Monitoring Program (VAMP), which monitors fraud and dispute levels across merchants. If your VAMP ratio exceeds Visa's thresholds, you risk fines, restrictions, or removal from the network.

Chargeback alerts let you refund a transaction and prevent the chargeback from landing, but by the time an alert is triggered, the issuer has already filed a fraud notice (TC40) with Visa. The dispute is resolved, but the TC40 still counts against your VAMP ratio.

Systematic Dispute Deflection intervenes earlier: because the dispute is blocked before it's created, the TC40 is never filed. You retain the funds, and the event is excluded from your VAMP calculation entirely. That makes it the only tool in the prevention ecosystem that addresses both the dispute and the associated fraud notice at the same time.

Systematic Dispute Deflection is powered by Visa's Compelling Evidence 3.0 and Mastercard's First Party Trust. As with Digital Receipts, ChargebackStop unifies both programs into a single interface.

Designed for Merchants, PSPs, and Acquirers

Like the rest of the ChargebackStop platform, these new capabilities are designed to work across the entire payments ecosystem.

For Merchants

Digital Receipts provide a clear record of purchases that helps customers recognize transactions and avoid unnecessary disputes. Systematic Dispute Deflection goes further by blocking first-party misuse disputes before they reach the network, protecting your dispute ratios and your VAMP standing without requiring you to refund the transaction.

For PSPs and Acquirers

Dispute deflection and enriched transaction data offer a scalable way to protect merchant portfolios from rising dispute ratios. Payment providers can deliver both capabilities as part of their existing merchant services, improving outcomes across the portfolio while reducing operational overhead.

For Platforms and PayFacs

White-label capabilities mean Digital Receipts and Systematic Dispute Deflection can be embedded directly into a platform's existing merchant tooling, strengthening merchant relationships and creating new service opportunities.

Built for Modern Payment Data

ChargebackStop has always approached chargeback management as a data problem. Better data leads to better outcomes. Digital Receipts and Systemic Dispute Deflection extend that philosophy by allowing merchants to provide richer order and transaction data to the dispute process.

The order information merchants submit through ChargebackStop's Orders API feeds both systems; richer order data means more qualifying identifiers are available for deflection, and more detailed receipts are available for bank-side lookups. This is why we recommend implementing both together.

Integration is straightforward, too. Merchants simply submit order data through ChargebackStop's existing APIs, and that data is automatically matched with alerts, disputes, and issuer queries. There's no need to build against either card network directly.

Prevention Keeps Moving Earlier

The payments industry has spent years treating chargeback management as a recovery problem, building evidence packs and fighting disputes after the fact. Alerts moved the intervention point earlier, and automation made that process scalable. Digital Receipts and Systematic Dispute Deflection represent the next step: resolving confusion and blocking illegitimate disputes before they enter the chargeback process at all.

Chargeback management works best when disputes never happen in the first place. If you'd like to see how these capabilities fit into your current setup, we'd be happy to show you. Book a demo or contact our team to learn more.