Understanding chargeback vs refund differences is crucial for businesses as chargebacks carry certain consequences for your business that are important to comprehend

This guide will explain how chargebacks and refunds work, the key differences between them, common reasons they are requested, and the most effective management and prevention strategies.

How Chargebacks and Refunds Work

While both chargebacks and refunds involve returning processed funds to customers, the implications are different for merchants.

Refund Process

When a customer requests a refund from the merchant directly, rather than the card-issuing bank, the product is reclaimed and their money is returned.

Implications of a Refund for a Merchant

The product may or may not be resold at full price as a consequence of the return, and the resource expenditure for the merchant involved: providing customer service, processing the refund, and processing the returned item.

Chargeback Process

When a customer requests a chargeback, they contact the card-issuing bank and their money is returned by being withdrawn from the merchant account, often with no notification to the merchant.

Implications of a Chargeback for a Merchant

The product may or may not be returned, and the resource expenditure for the merchant involved: returning the customer’s money, paying a chargeback processing fee, and forfeiting the product.

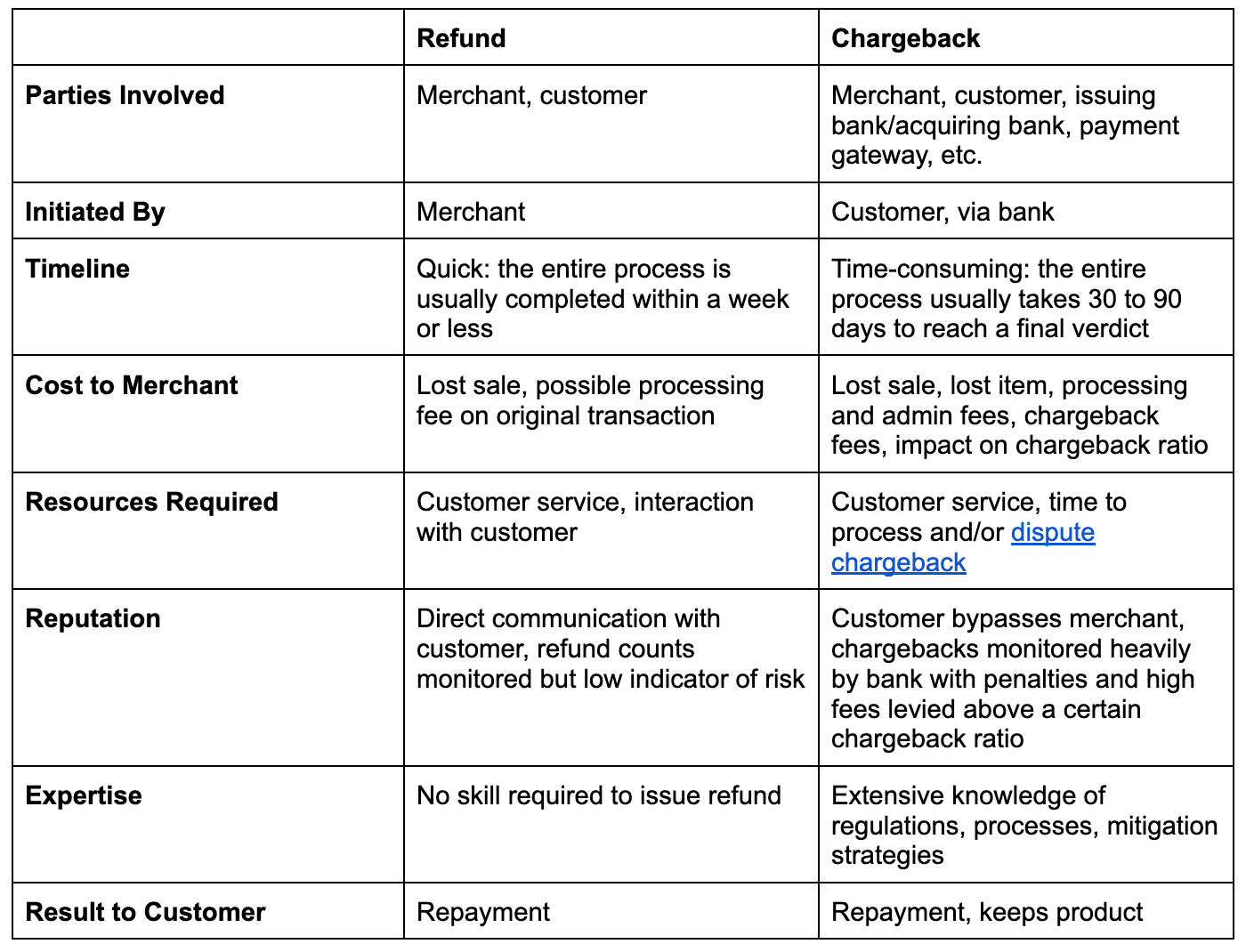

Key Differences (Chargebacks vs Refunds)

While both chargebacks and refunds represent a net loss for merchants, chargebacks are significantly more costly for merchants.

Refunds mean there are no intermediaries and the merchant can interact directly with the customer, with more control of the process and insight into the claim.

Chargebacks take longer, involve more expertise to dispute, present reputational risks with customers and the issuing bank, and cost more due to processing and chargeback fees.

Below are the key differences across several factors:

Related: What's the Difference Between a Refund and a Reversal?

Why Do Customers File Chargebacks Instead of Requesting Refunds?

Customers often choose to file a chargeback instead of requesting a refund directly from the merchant—sometimes even when a refund would have been easier for everyone involved.

Here’s why that happens:

- Lack of clear refund policy: If customers can’t easily find your refund policy or it’s hard to understand, they may feel their only option is to contact their bank.

- Missing or confusing contact details: Without obvious ways to reach you (like a support email or phone number), customers may not feel confident you’ll resolve their issue.

- Perceived convenience: Some customers see chargebacks as a “one-click” fix, especially if they’ve had poor experiences dealing with merchants in the past.

- Fraud concerns: If a customer doesn’t recognize your business name on their statement or suspects unauthorized activity, their first instinct may be to dispute the charge with their bank.

- Emotional reaction: Frustrated customers are more likely to skip communication with the business altogether and go straight to their card issuer.

The best way to avoid this? Clear communication, excellent customer service, and a simple refund experience that builds trust before tensions escalate.

Common Reasons for Chargebacks and Refunds

Refunds often spill over to chargebacks due to poor customer service or inadequate information regarding the return policy and process on the merchant’s website.

Chargebacks

Customers may go directly to their card issuer to resolve a disputed payment if they:

- Don’t recognize a purchase on their statement

- Can’t find or understand the refund policy

- Can’t find contact information for the merchant

- Are unwilling to engage with the merchant

- Want a one-stop resolution rather than contacting merchants individually in case of fraud

Refunds

If a customer finds a refund policy and chooses to request a refund from the merchant, common reasons may include:

- Defective products

- Poor quality

- Wrong items

- Late delivery

Preventing Honest Chargebacks and Refunds

There are several legitimate reasons that customers request chargebacks or refunds.

To prevent issues before they affect your bottom line:

- Visibly state contact information options on your website to address potential complaints before they escalate

- Make your refund policy as clear and straightforward as possible. Bringing awareness to your policy and making it as frictionless as possible will make customers less likely to trigger chargebacks out of convenience.some text

- Consider providing a FAQ section if it helps simplify your policy

- Use recognizable billing descriptors so customers can recognize your brand when it appears on their monthly statementssome text

- If your company name is significantly different than product names, notify your customers how the transaction will be labeled after a purchase

- Provide excellent customer service. Make it easy for customers to resolve queries, while improving customer satisfaction and collecting additional information for quality control.

- If yours is a physical product, invest in a reliable delivery service to ensure items arrive on time and undamagedsome text

- Consider simplifying your shipping policies

Other helpful tips to consider:

- Proactively monitor social media platforms for mentions of complaints against you

- Employ a chatbot if you need to serve customers at scale

- Ensure your Terms and Conditions are updated and intelligible

Reducing Fraudulent Chargebacks and Refund Abuse

A small amount of “friendly fraud” (customers buying items with the intent to dispute charges after the fact) and chargebacks are to be expected for any online merchant.

To reduce these types of chargebacks and refunds:

- Require additional verification during checkout. This may include three-digit card verification values (CVVs), or 4-digit card identification numbers (CID) on credit cards.

- Use address verification systems (AVS) to match a customer’s billing address with their information on file at the card-issuing bank.

- Use fraud management filters or tools that flag purchases from suspicious cards in unverified locations.

- Disable guest checkout to trace purchases back to logged in users.

What are Double Refunds?

Double refunds occur when customers collect two repayments, through both a chargeback and a refund. This means double the revenue loss for a merchant, plus any chargeback fees.

Double refunds may be initiated in two cases:

- Deliberately by friendly fraudsters contacting both their bank and the merchant about obtaining a refund

- Accidentally by honest customers taking action on both fronts where the refund policy or language around the process is unclear

To remediate this, merchants must go through chargeback recovery, which involves presenting evidence to the issuing bank that they already issued a refund themselves.

ChargebackStop Chargeback Protection

Chargeback protection is important to reduce post-chargeback risks for your business.

ChargebackStop protects against all chargebacks globally– per alert, not transaction.

ChargebackStop also reduces your chargebacks by 99%.

To see our chargeback prevention platform in action, visit ChargebackStop.com and sign up for a free demo.

Do you still have questions? We’re happy to help you figure all this stuff out.

Visit ChargebackStop.com/contact-us for sales or support.

FAQ

Are chargebacks and refunds the same?

Though both may appear the same to a customer who gets their money back, chargebacks are issued by the issuing bank whereas refunds are issued by merchants. This difference is crucial since chargebacks involve processing fees, penalties, and reputational risk for merchants.

What are common reasons for refunds?

Common reasons for refund requests are customer dissatisfaction with the product or service, errors in billing, or the customer receiving damaged or wrong items.

Why are refunds preferable to chargebacks for merchants?

Issuing refunds before they turn into chargebacks are quicker, cheaper, and within the merchant’s control. By dealing with customers directly, merchants avoid chargeback processing fees and penalties

Refunds are also much quicker to issue and have no impact on the merchant’s chargeback ratio, which impacts their standing with their bank.

Lastly, by speaking to customers directly, merchants can improve their customer satisfaction by volunteering to help and demonstrating goodwill.

Can both refunds and chargeback happen simultaneously?

Yes. This is known as a double refund, and it will require merchants presenting evidence to the issuing bank of a previous refund to recover the payment.

What is a reversal?

A reversal revokes previous transactions. This happens when a business doesn’t receive an authorization response, or a card transaction is voided or canceled.

How are refunds different from reversals?

The difference is in the timing of the transaction.

Refunds are repayments of money after a transaction is finalized and the funds are settled.

Reversals are automated processes triggered by a bank to cancel a transaction before it is finalized. This happens before a transaction is fully completed, when the funds are not yet settled.