The Visa Acquirer Monitoring Program (VAMP) has historically helped Visa safeguard the integrity of its payment system through two key frameworks: the Visa Dispute Monitoring Program (VDMP) and the Visa Fraud Monitoring Program (VFMP).

Under these programs, Visa monitored transactions to detect and prevent fraudulent behavior and disputes. Visa also placed significant responsibilities on acquirers and merchants to comply with their standards and avoid excessive chargebacks.

This all changed on April 1st, 2025 when the VDMP and VFMP were retired and replaced with an updated and consolidated VAMP framework.

How the Previous Visa Acquirer Monitoring Program Worked

VAMP previously encompassed two distinct frameworks: VDMP and VDFP.

VDMP targeted high chargeback rates across all dispute types and aimed to mitigate disputes between customers and merchants. In contrast, VFMP focused on detecting and preventing fraudulent activities from consumers.

The programs differed in their metric calculations, with VDMP using a dispute ratio based on the number of disputes compared to total transactions, and VFMP calculating a fraud rate based on the total dollar value of fraudulent transactions compared to legitimate ones.

The two programs also had different thresholds. VDMP's standard threshold was a 0.9% dispute ratio with at least 100 total disputes, while VFMP's standard threshold was a 0.9% fraud rate with at least US $75,000 in total fraud.

How the Visa Acquirer Monitoring Program Changed

Visa consolidated the VDMP and VFMP frameworks under a single Visa Acquirer Monitoring Program on April 1st. Visa’s ultimate goals remain the same—to track, manage, and reduce activity related to fraud and chargebacks—but there are some changes to thresholds for disputes and fraud.

These were revised in May 15 with an effective date of June 1, 2025:

- Merchants in most regions have an initial threshold of 2.2%, dropping to 1.5% from April 1, 2026. The exception for this is LATAM and Caribbean merchants, whose threshold is already set at 1.5%.

- Acquirers have slightly different thresholds. The Above Standard threshold is set at 0.5%-0.7%, with anything above 0.7% being classified as Excessive.

These new thresholds only apply to merchants when the total number of fraud transactions and non-fraud disputes is:

- Greater than 1,500 (outside MENA); or

- Greater than 100 and over US$75,000 in value (inside MENA).

Day-to-day, not much has changed. Just like under the previous VDMP and VFMP frameworks, acquirers and merchants should be proactive in their compliance efforts to ensure that they don’t exceed these thresholds and be forced to join the program.

That said, the new thresholds are much stricter, beginning at ratios of 0.3% for acquirers. Notably, the Early Warning program has also been eliminated, illustrating that Visa intends to increase the pressure on acquirers and merchants to get their compliance affairs in order.

Visa also introduced a separate enumeration ratio. An enumerated transaction, also known as card testing fraud, is a type of fraud that uses a combination of values to guess payment information. The enumeration ratio applies to enumeration attacks identified by Visa’s Account Attack Intelligence system. Under the new VAMP framework, the excessive enumeration program will be triggered when:

- More than 300,000 enumeration attacks are identified in a calendar month; and

- Those attacks constitute 20% or more of total transactions (approved and declined).

The enumeration ratio can be calculated as follows:

Enumerated transactions ÷ Total sales count

What These Changes Mean for Acquirers and Merchants

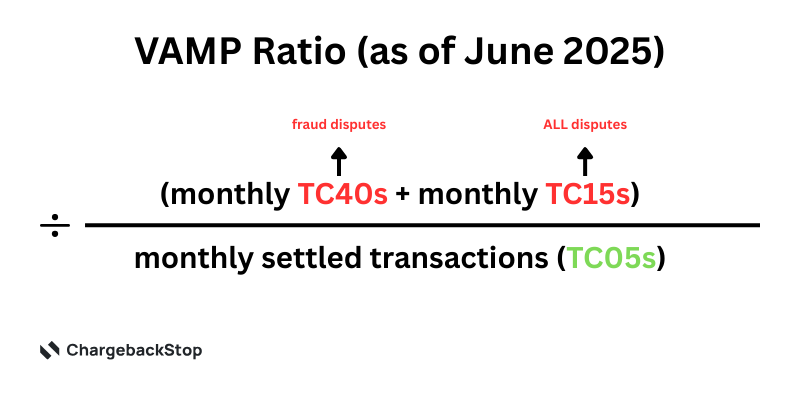

Ultimately, the updates to VAMP are designed to streamline the management and mitigation of chargebacks and fraud. Acquirers and merchants will now have only one dispute ratio to keep track of, the new VAMP ratio:

Merchants need to be particularly mindful that while their new VAMP ratio threshold is currently set at 2.2%, this will drop to 1.5% from April 1, 2026. Visa has also changed their position regarding the counting of TC40s and TC15s. It was initially the case that only non-fraud chargebacks were counted in the ratio, but TC15s have now been updated to include all chargebacks, not just non-fraud ones.

In practice, this means that a fraud report (TC40) that then becomes a fraud chargeback will be counted twice, both as a TC40 and a TC15. This will increase VAMP ratios for most merchants and acquirers because if 3-D Secure is not used, every TC40 should also lead to a fraud chargeback.

That said, TC15 disputes avoided via CDRN and Rapid Dispute Resolution (RDR) will not be counted in VAMP ratios. While RDR will not block TC40s, it will cancel out TC15s for both fraud and non-fraud cases if they are resolved before becoming chargebacks. This makes an extremely strong case for all merchants and acquirers to adopt RDR and other pre-chargeback processes, because it can help them avoid the double-counting impact of TC40 + TC15.

Penalties for Non-Compliance

Visa is changing the penalties it levies against acquirers and merchants for breaching the new rules. For the first six months of VAMP, Visa is providing a grace period before enforcing fines.

Following this grace period, merchants and acquirers that breach VAMP thresholds will be placed in the program and incur fines for each subsequent transaction that’s disputed or reported as fraud.

VAMP Introduction and Enforcement Timeline

Visa is taking a staged approach to introducing the new iteration of VAMP. These are the key dates you need to be aware of:

- March 31st, 2025: Current VFMP and VDMP frameworks were retired.

- April 1st, 2025: The updated and consolidated VAMP framework launched.

- June 1st, 2025: Updates to the thresholds and VAMP Ratio came into effect.

- October 1st, 2025: The grace period for assessing fines expires.

- April 1st, 2026: Fraud and dispute thresholds decrease.

Your Next Steps

Acquirers and merchants both have roles to play in strengthening their operations against fraud and chargebacks.

While acquirers have more skin in the game because of the overarching responsibility for the performance of their merchant portfolios, merchants still need to adjust their fraud prevention and dispute management practices to avoid falling foul of VAMP thresholds. Indeed, merchants may find that their acquirers impose limits below Visa’s 0.9% threshold to compensate for their lower thresholds (beginning at 0.3%).

To make sure you’re not caught out by these changes to VAMP (and the inevitable changes that will come in the future), start assessing and strengthening your existing compliance posture by taking steps like:

- Monitoring your current chargeback and fraud ratios.

- Strengthening fraud prevention by implementing filters and authentication methods.

- Using alert tools like Visa’s RDR and Verifi’s CDRN.

- Implementing third-party chargeback management solutions.

- Engaging with others in your network to learn about their systems support compliance.

All in all, these changes point toward one clear message from Visa: Acquirers and merchants need to tighten their ships by introducing more robust compliance practices and taking steps to reduce instances of fraud and chargeback disputes. Those who fail to respond will find themselves subject to mounting fines, reputational damage, and, for merchants, potential account terminations by their acquirers.

Take Control of Your Disputes with ChargebackStop

With Visa’s changes to its Acquirer Monitoring Program, chargebacks are becoming even more costly and damaging for merchants. That’s why it’s more important than ever for merchants to take a preventative rather than reactive approach to chargeback management.

The ChargebackStop platform helps merchants automatically prevent chargebacks using tools like Ethoca Alerts and Verifi RDR, and effortlessly recover lost revenue through streamlined representment.

- Same-day setup: Get started instantly with automatic volume pricing.

- All-in-one platform: Manage Visa RDR and Mastercard Ethoca alerts in a single streamlined dashboard.

- Hands-free automation: No need for manual monitoring or adjustments. Our system applies the best industry practices for chargeback prevention.

For merchants looking to stay ahead of chargebacks and improve fraud prevention among an increasingly punishing compliance environment, adopting ChargebackStop is a smart move. Get started today and take control of your dispute management process.